- S&P 500 contracts climb; China Evergrande concerns linger

- WTI crude oil rises and iron ore rout eases; dollar steady

Stocks in Europe advanced along with U.S. index futures on Tuesday as traders reassessed risks from China’s crackdown on the real-estate sector and looked ahead to this week’s Federal Reserve meeting.

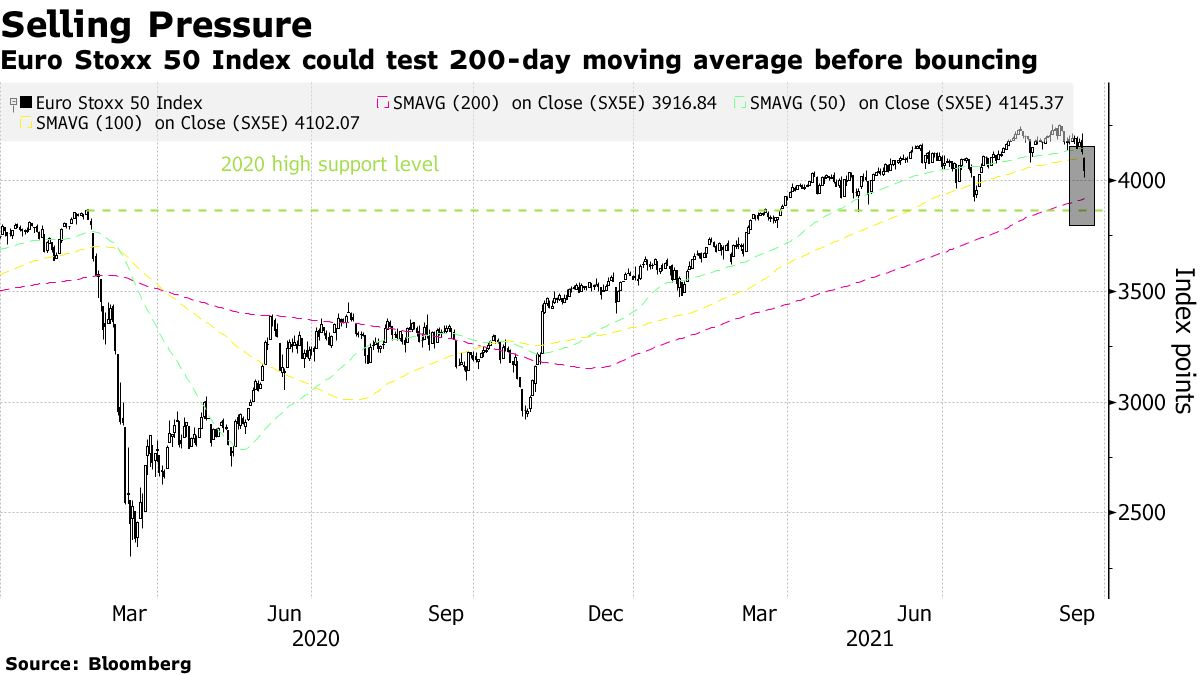

The Stoxx Europe 600 index climbed more than 1%, rebounding from the biggest drop in two months, with energy companies leading the advance and all industry sectors in the green. Royal Dutch Shell Plc rose after the company offered shareholders anpayoutfrom the sale of shale oil fields. Universal Music Group BV sharessoaredin their stock market debut after being spun off from Vivendi SE.

Futures on the S&P 500 and Nasdaq 100 gained, suggesting some improvement in sentiment after concerns about fallout from China Evergrande Group’s debt woes roiled markets Monday.Dip-buyersin the last hour of trading Monday helped the S&P 500 pare some losses, though the index still posted the biggest drop since May.

Aside from worries over Evergrande’s ability to make good on $300 billion of liabilities, investors are also positioning for the two-day Fed meeting starting Tuesday, where policy makers are expected to start laying the groundwork for paring stimulus. Treasury yields rose and the dollar was steady.

“So much of this information is already known that we don’t think it will necessary set off a wave of problems,” John Bilton, head of global multi-asset strategy at JPMorgan Asset Management, said on Bloomberg TV. “I’m more concerned about knock-on sentiment at a time when investor sentiment is a bit fragile. But when we look at the fundamentals -- the general growth, and direction in the wider economy -- we still feel reasonably confident that the situation will right itself.”

Elsewhere, Bitcoin slid for a third day in volatile trading, tumbling as much as 7.6% before bouncing back to above $43,000. Oil rebounded from two days of declines, while iron ore futurestook a breatherfollowing Monday’s rout, though stayed below $100 a ton on China’s steel output curbs.

In Canada, Prime Minister Justin Trudeau won a third term in a snap election but fell short of regaining a parliamentary majority. The nation’s currency was among the best performers in the Group-of-10 basket.

Here are key events to watch this week:

- Bank of Japan rate decision, Wednesday

- Federal Reserve rate decision, Wednesday

- Bank of England rate decision, Thursday

- Fed Chair Jerome Powell, Fed Governor Michelle Bowman and Vice Chairman Richard Clarida discuss pandemic recovery, Friday

Some of the main moves in markets:

Stocks

- The Stoxx Europe 600 rose 0.9% as of 10:17 a.m. London time

- Futures on the S&P 500 rose 0.8%

- Futures on the Nasdaq 100 rose 0.7%

- Futures on the Dow Jones Industrial Average rose 0.9%

- The MSCI Asia Pacific Index fell 0.4%

- The MSCI Emerging Markets Index rose 0.1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%

- The euro was little changed at $1.1735

- The Japanese yen fell 0.1% to 109.55 per dollar

- The offshore yuan rose 0.1% to 6.4756 per dollar

- The British pound rose 0.2% to $1.3687

Bonds

- The yield on 10-year Treasuries advanced two basis points to 1.33%

- Germany’s 10-year yield advanced one basis point to -0.31%

- Britain’s 10-year yield advanced one basis point to 0.80%

Commodities

- Brent crude rose 1.3% to $74.89 a barrel

- Spot gold was little changed