Post-Earnings Plunge: LRCX Cautious Q2 Guidance Sparks AI Optimism vs. Geopolitical Fears Debate

$Lam Research(LRCX)$ released its Q1 FY2026 earnings report (ending September 28, 2025), delivering solid results while facing short-term cyclical fluctuations and macroeconomic uncertainties. Specifically, revenue and EPS both slightly exceeded expectations, while gross margin and operating margin hit all-time highs, reflecting robust resilience amid AI-driven semiconductor equipment demand. The overall performance was "excellent," with key highlights including robust demand for AI-related high-end deposition and etching equipment, driving growth in foundry and memory businesses. Potential concerns stem from the short-term impact of export restrictions to China and the slight sequential decline indicated in guidance, which may reflect industry cyclical fluctuations and geopolitical uncertainties.

Investors remain cautious and are increasingly focused on taking profits. The sharp post-market price fluctuations may stem from the market's conservative interpretation of future guidance.

Key Financial Highlights

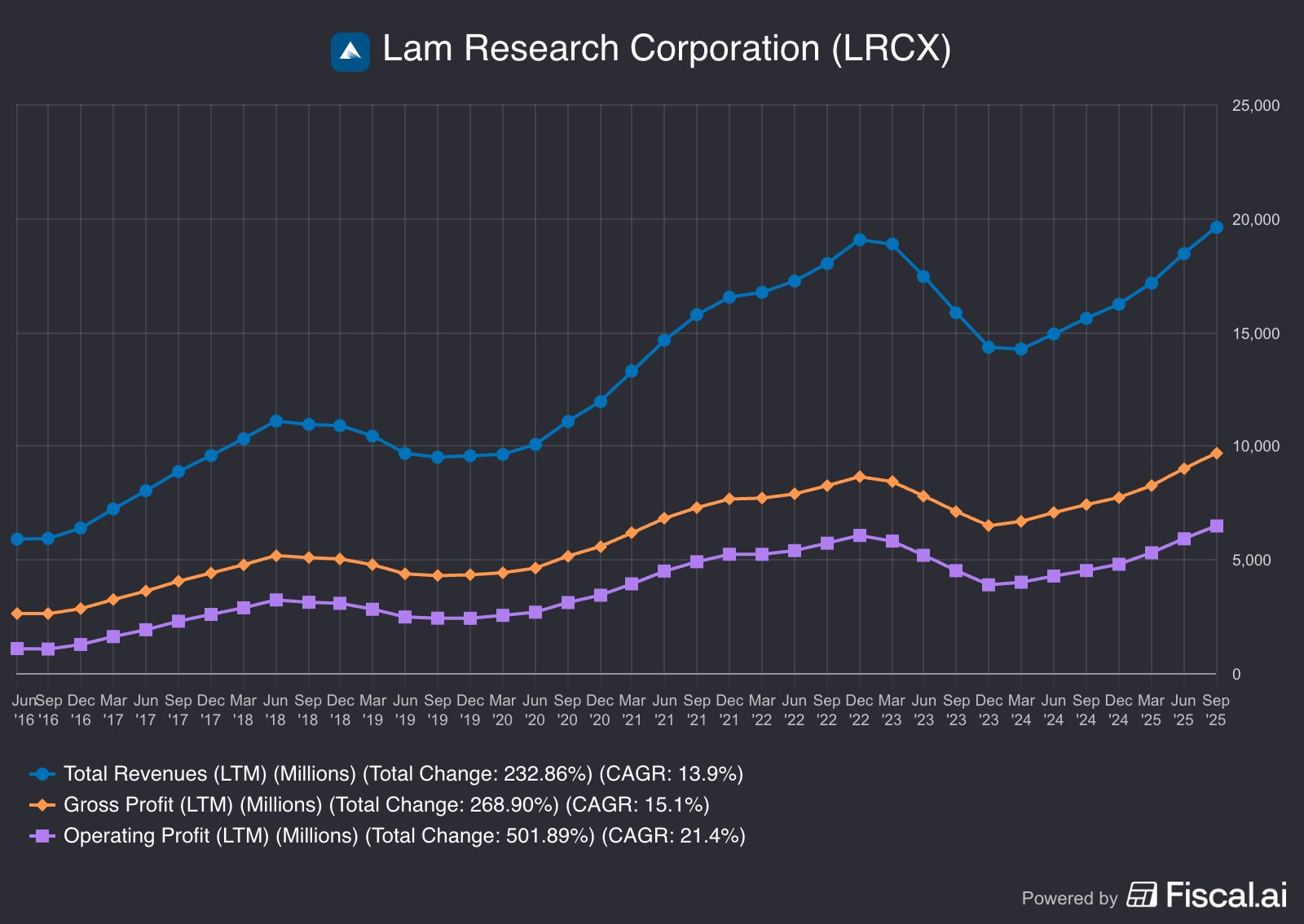

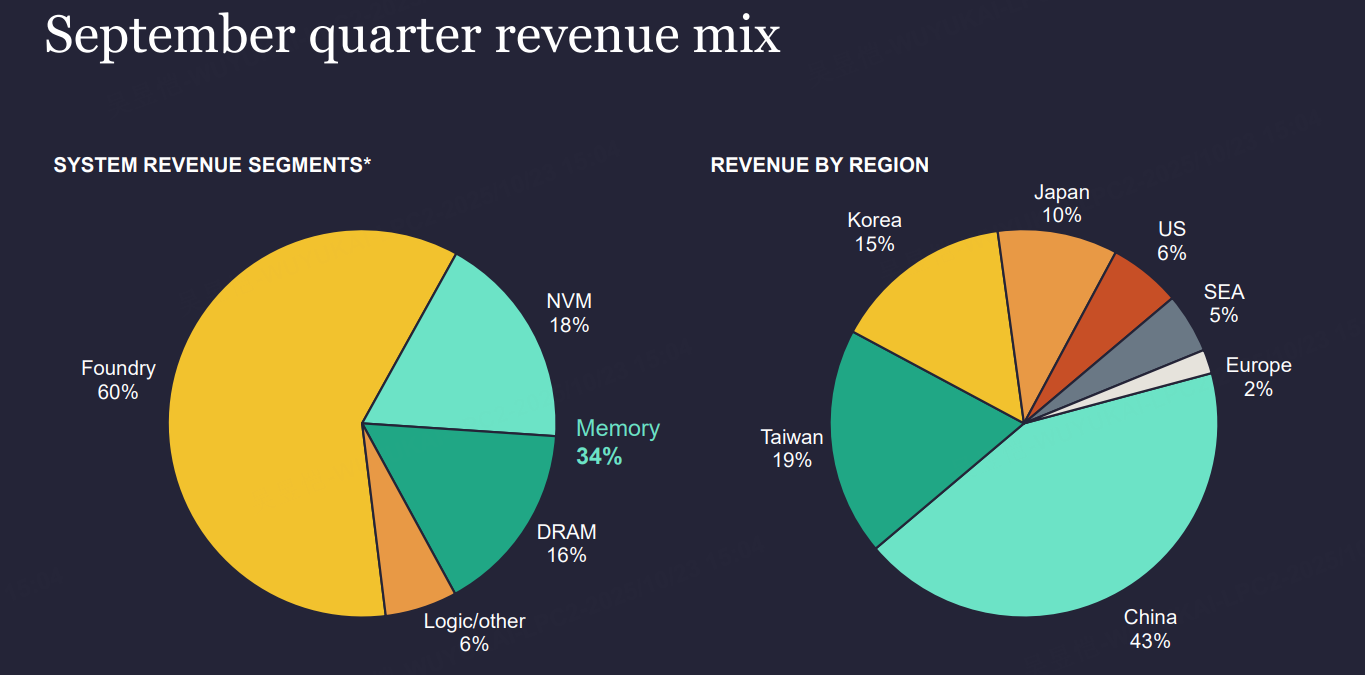

Revenue reached $5.32 billion (up 3% quarter-over-quarter, approximately 25% year-over-year). This figure exceeded the market consensus of $5.22 billion, driven primarily by investment in AI infrastructure, particularly growth in demand for high-bandwidth memory (HBM) and advanced packaging, which boosted the proportion of revenue from the systems business. The outperformance was notable, especially as foundry business share rose to 60% (from 52% last quarter). However, China accounted for a significant 43% of revenue, and future restrictions may constrain overall growth. Signs of business structure shift: Customer Support Business Group (CSBG) revenue reached $1.78 billion, representing about 33% of total revenue, indicating strengthened stable cash flow contributions from services and spare parts operations.

EPS of $1.26 (down 5.3% quarter-over-quarter, up approximately 42% year-over-year). This exceeded market expectations of $1.22, primarily driven by record-high gross margin of 50.6% and operating margin of 35%. These efficiency gains stemmed from optimized product mix and cost control. The sequential decline from the prior quarter's $1.33 may stem from seasonal factors and some supply chain pressures. Structural shift: Memory business (NAND+DRAM) accounted for 34% of revenue, with DRAM benefiting from AI SSD demand, signaling the company's transition from traditional cyclicality toward AI-driven structural growth.

Cash Flow and Shareholder Returns: Strong operating cash flow, with dividends and share repurchases totaling $1.282 billion.

Cash balance reached $6.7 billion, remaining stable quarter-over-quarter. This was driven by improved profitability and optimized inventory management. The excess over expectations was reflected in a $99 million share repurchase, demonstrating management's confidence in the stock price. Structural changes: CSBG's annual growth projections reinforced the proportion of recurring revenue, supporting the company's evolution from equipment sales toward a service platform model.

Future Signal

Management expressed an overall optimistic outlook for fiscal year 2026 during the earnings call, but guidance indicates second-quarter revenue (ending December) of $5.2 billion ± $300 million, with earnings per share of $1.15 ± $0.10. gross margin of 48.5% ± 1%, and operating margin of 33% ± 1%. This represents a slight sequential decline and is characterized as "conservative" guidance aimed at managing market expectations and mitigating geopolitical risks.

CEO Tim Archer emphasized that "AI and its impact on the semiconductor industry remain a key focus, with announced data center CapEx investments expected to drive significant expansion of manufacturing capacity over the coming years."

This statement leans toward optimistic reassurance, logically emphasizing AI's multi-year growth potential while pragmatically acknowledging the impact of China's restrictions (Q2 revenue hit of $200 million, full-year 2026 impact of $600 million). CFO Doug Bettinger added: "We expect to deliver record financial performance in 2025." This phrasing strikes a pragmatic tone, emphasizing record profitability without overpromising, while implicitly reflecting caution regarding industry volatility (such as cleanroom capacity constraints).

Key Points for Investors

Sustainable long-term growth opportunities primarily include AI-driven deposition/etching and advanced packaging equipment, as well as NAND upgrades (projected $40 billion in WFE spending). These sectors rely on structural demand driven by data centers and HBM, rather than short-term cycles. In contrast, traditional logic/other businesses (accounting for only 6% of revenue) are more susceptible to macroeconomic sentiment, such as slowing economic recovery, and may face volatility in non-AI segments. We believe that compared to previous quarters, the increased share of foundry equipment and slight rise in DRAM share confirm Lam's transformation from a cyclical equipment supplier to a core provider of AI infrastructure—similar to NVIDIA's evolution from a GPU supplier to a full-stack AI platform.

Management's overall strategy remains sound, though certain missteps exist—such as excessive reliance on the Chinese market (43%)—warranting accelerated diversification before Q2. Key areas for amplified investment include AI-related R&D and driving product evolution toward platformization, such as enhancing CSBG's service ecosystem. Signals indicate the company is moving toward horizontal expansion, such as entering more AI sub-sectors through advanced packaging technology and deepening collaborations with partners like NVIDIA. This may signal a shift from devices to integrated solutions, similar to Booking's evolution from hotel reservations to a travel platform.

The current valuation (assuming a share price of approximately $145 and a P/E ratio of about 25x) implies expectations for roughly 20% EPS growth in fiscal year 2026. Market pricing appears largely justified, particularly within the AI theme, though declining China revenue may be underestimated, potentially causing short-term volatility. Compared to peers like Applied Materials (AMAT, with a similar P/E but lower exposure to China) and KLA Corp (KLAC, focused on metrology equipment), Lam Research has a stronger AI positioning yet commands a modest valuation premium. Its undervaluation may lie in CSBG's recurring revenue, as the market may not fully price in its platform potential.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-10-23Current quarter guide is very strong, then guided strong growth but backloaded next year. decrease in china contribution but more than made up by ROW.LikeReport

- Merle Ted·2025-10-23Every 100b in data center spend translates to 8b WFE spend = LRCX $250 middle of 2026LikeReport

- doozi·2025-10-23It's fascinating how LRCX is navigating these complexitiesLikeReport