Unity Q2 Earnings: Profit Turnaround Confirmed, But Why Did Shares Drop?

$Unity Software Inc.(U)$ Q2 confirmed the profitability inflection point (improved EBITDA and cash flow) and technology inflection point (Vector performance), but a full-scale revenue rebound will require waiting for H2 price increases to materialize and Vector cross-product line reuse. Short-term valuation is anchored in the $157-183B range, and whether it can break through the upper limit depends on:

Can Vector replicate $AppLovin Corporation(APP)$ 's closed-loop ecosystem?;

Monetization efficiency of Unity 6's replacement strategy in China;

Non-gaming industry orders surge.

Q3 focuses on three key metrics: ad network growth, Unity 6 penetration rate, and China region contribution, to validate management's "turning point" narrative.

Performance and market feedback

Key performance indicators

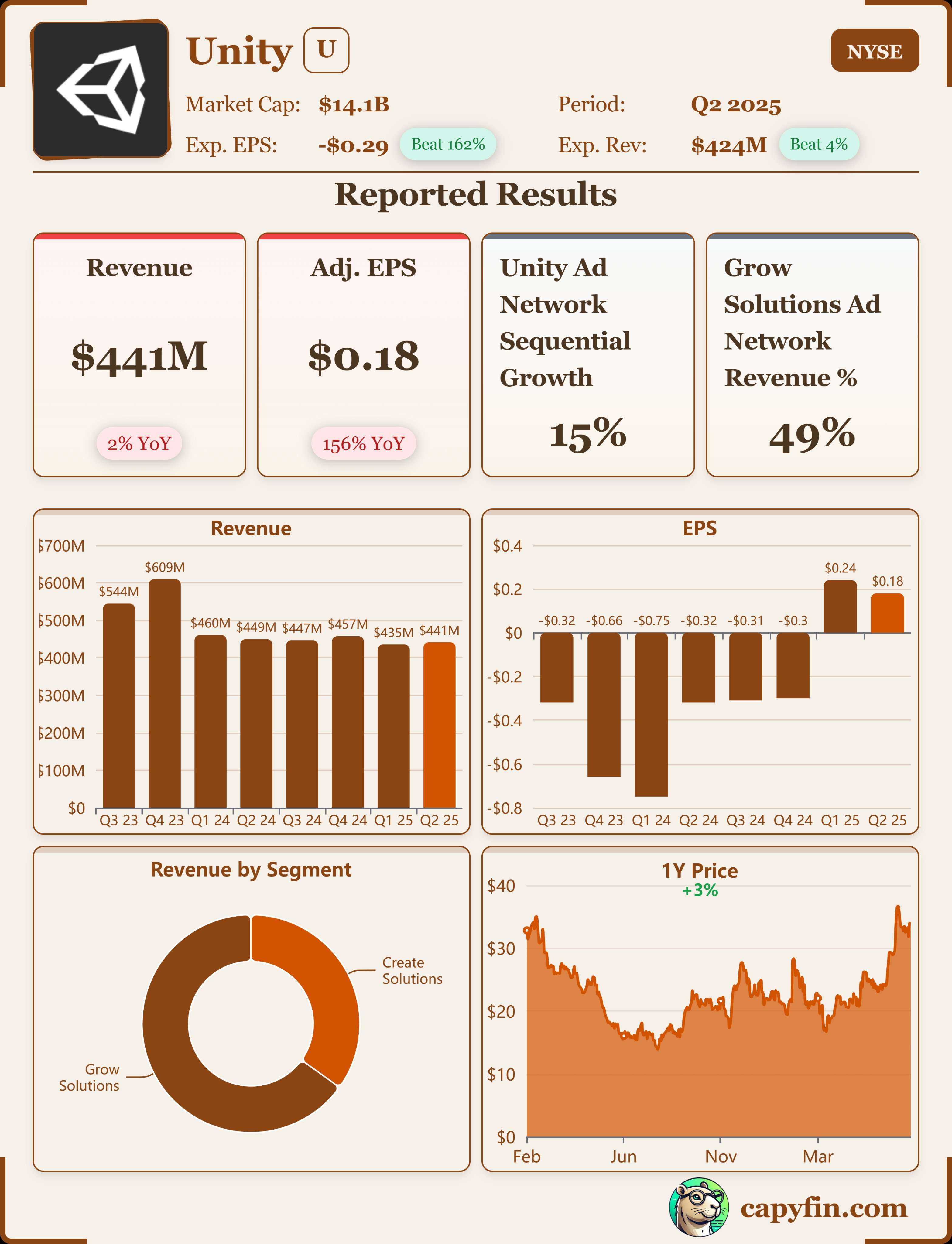

Second-quarter revenue was $441 million, down 2% year-over-year (Q2 2024 was $449 million), but exceeded market expectations of $426.8 million by approximately 3.3%. The decline in revenue was primarily due to weak performance of Grow Solutions' non-ad network products, but was partially offset by strong growth in Unity's ad network (up 15% quarter-over-quarter) and stable performance in Create Solutions (up 2% year-over-year). China Market: Revenue increased by $20 million quarter-over-quarter, emerging as a growth highlight.

Adjusted EBITDA of $90 million (margin of 21%, $15 million); free cash flow of $127 million (cash increased to $1.7 billion)

Create Solutions: Revenue of $154 million, up 2% year-over-year and up 2% quarter-over-quarter, driven primarily by double-digit growth in term license sales (approximately $12 million) and subscription revenue, partially offset by declines in non-strategic professional services and consumer services.

Grow Solutions: Revenue of $287 million, down 4% year-over-year and up 1% quarter-over-quarter, with Unity's ad network accounting for 49% of revenue, up 15% quarter-over-quarter, but other ad products underperforming.

market response

Following the release of its financial report, Unity's stock price rose 11.33% in pre-market trading to $37.78, approaching its 52-week high of $38.96, indicating market confidence in the company's AI strategy and growth prospects. However, the stock then opened higher but closed lower during the trading session, ultimately ending the day down 5.95%, reflecting market concerns over the company's high debt levels and the stability of its non-advertising network business.

Key Investment Points

Will Vector drive a turning point in the advertising business? The ecosystem barrier remains weaker than that of competitors.

AI advertising platform Unity VectorQ2 has completed a full migration, with ad conversion rates increasing by 15%-20%, driving a 15% quarter-on-quarter increase in ad network revenue. 85% of top mobile game clients have already adopted the platform. The technical differentiation lies in the use of player behavior data within the engine (such as scene attention peaks) to dynamically optimize bidding and improve advertisers' ROAS.

Currently, Vector's bottleneck is that its data closed loop is weaker than Applovin's (Axon model), mainly due to a lack of first-party game data and non-full-stack advertising technology (no proprietary DSP), which limits the extraction of ecosystem value. Non-ad network products (accounting for 50% of Grow's revenue) remain weak, dragging down overall growth.

Create business strategy transformation takes effect, pricing power and penetration rate both increase

After stripping out low-margin professional services revenue, subscription revenue accounted for 80% of total revenue, driving the gross margin up to 83%, establishing it as the dominant business model; the price increase for the Unity 6 engine has yielded benefits, with 43% of active users already upgrading (target of 70% by the end of 2025), and the price increase effect is expected to be fully realized in H2. Breakthrough in non-gaming scenarios: Expanding into automotive (BMW, Mercedes-Benz), healthcare (Specto), and industrial simulation (Raytheon) clients to mitigate risks associated with market saturation in the gaming industry.

Although Q2 revenue was boosted by a large customer transaction (approximately $12 million), Q3 may see a slight sequential decline. However, CFO Jarrod Yahes emphasized that, excluding one-time factors, strategic revenue is expected to achieve high single-digit year-over-year growth in Q3. This indicates Unity's continued progress in its subscription and platform strategy.

China Strategy: Localization Replacement and Growth Engine

Unity 6 is based on the Chinese version of the "Unity Engine," which has been optimized for rendering functionality and has secured partnerships with major clients such as Tencent (Q2 saw the addition of a multi-year contract). The China region saw a $20 million increase quarter-over-quarter, making it the only market globally with single-digit growth. The company's long-term partnerships with Tencent and Scopely, as well as its collaboration with Nintendo on the Switch 2 project, highlight its strategic position within the global gaming ecosystem. Additionally, Unity's expansion into the automotive (BMW, Mercedes-Benz) and healthcare (Specto Medical) sectors has opened up new non-gaming revenue streams.

Profitability turning point confirmed, improved cash flow supports deleveraging

Adjusted EBITDA margin reached 21%, exceeding expectations and reflecting the company's progress in cost control and operational leverage. Adjusted gross margin was 83%, demonstrating an efficient cost structure. Free cash flow was $127 million, up 58.75% year-over-year (Q2 2024 was $80 million), providing ample funds for the company to invest in AI and product innovation.

Cost optimization has peaked, and restructuring dividends have faded (GAAP expenses down 5% year-on-year). Future profit margin growth will depend on advertising revenue growth.

Balance sheet repair, free cash flow of $127 million boosts net cash reserves, management clearly prioritizes debt repayment (net debt of $7.21 billion).

Performance guidance and tone

Q3 growth acceleration signals are clear, with revenue guidance of $440-450 million (QoQ +2-4%), marking the highest level since Q4 2023. Among these, Grow: Mid-single-digit QoQ growth (ad network continues double-digit growth). Create: Excluding the impact of large customer orders in Q2, strategic revenue is expected to grow at a high single-digit rate year-over-year. Profitability: Adjusted EBITDA of $90-95 million (margin ~21%), with operational leverage beginning to emerge.

CEO Bromberg positions Q2 as a "turning point," emphasizing three key drivers: Vector's outperforming expectations, Unity 6 price increases, and partnerships in China (Tencent, Scopely, Nintendo Switch 2).

Seller's core dispute

Vector scalability: Can it be expanded from the advertising network to other Grow products? Management responded that the modular design supports rapid reuse.

Sustainable growth: Will H2 price increases drive Create acceleration? Can China's contribution be sustained?

Competitive barriers: The pace at which the technological gap with Applovin is narrowing.

Valuation anchors and repricing triggers

Current division valuation:

Main catalyst:

Upward repricing: Vector conversion rate consistently >20%, Unity 6 penetration rate exceeds 70%, non-game revenue share exceeds 30%.

Downside risks: Advertisers' budget migration is not as expected, and price increases lead to the loss of small and medium-sized developers.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Valerie Archibald·2025-08-08We're on our way to $40.LikeReport

- Venus Reade·2025-08-07PT raised. Held the gap. Let’s see what U will do in the upcoming months and years.LikeReport

- Merle Ted·2025-08-07Don't mind if it falls. It will stand up againLikeReport

- HilaryWilde·2025-08-07Turning pointLikeReport