Wall Street PANICS: Did $740M Missing Cash Sink PayPal Stock?

Core Performance and Market Feedback

Revenue and EPS performance: PayPal Q2 2025 revenue of $8.29 billion, up 5% y-o-y, exceeding market expectations of $8.08 billion; non-GAAP EPS of $1.40, +29.6% y-o-y, higher than expectations of $1.30, demonstrating significant improvement in profitability.

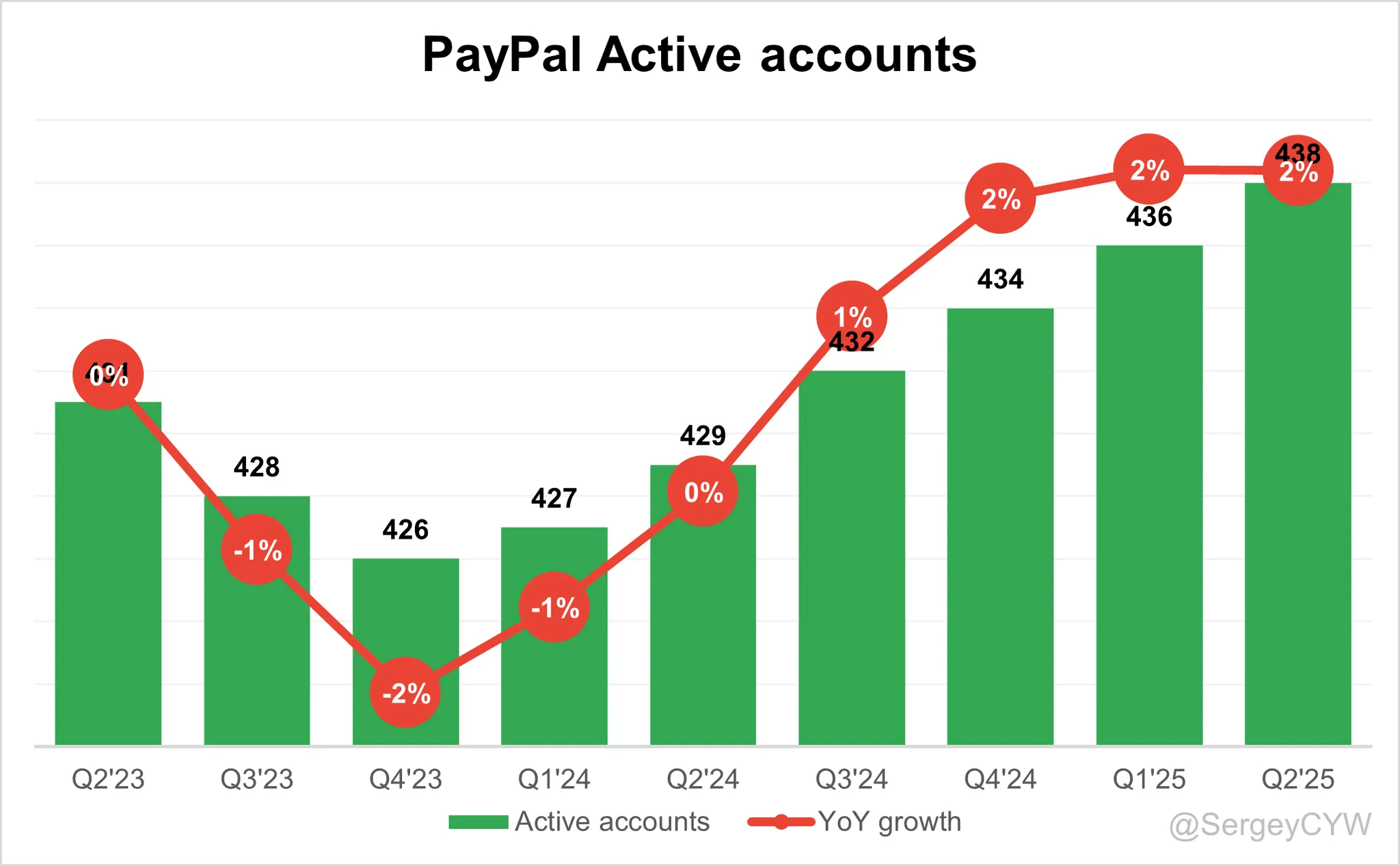

Key operating metrics: total payment volume (TPV) reached $44.36 billion, up 6% y/y, active accounts increased to 438 million, +2% y/y; trading profit increased 7% y/y to $3.84 billion, but slowed down slightly from Q1.

Earnings guidance and tone: the company raised full-year non-GAAP EPS guidance to $5.15-5.30 (previously $4.95-5.10), Q3 EPS guidance of $1.18-1.22 slightly below market expectations of $1.20; management's tone was positive, emphasizing AI, cryptocurrencies and global expansion potential.

However, adjusted free cash flow was only $656 million, well below expectations of $1.4 billion, and plummeted 53% sequentially from Q1, likely dragged down by a sequential increase in operating expenses ($6.78 billion vs. $6.26 billion in Q1) and restructuring costs.

Shares fell 8.66% to $71.45 (versus $78.22 prior) on July 29 following the earnings release, reflecting investor concerns about declining free cash flow ($656 million, well below expectations of $1.4 billion) and conservative Q3 guidance.The decline in free cash flow could also reduce the company's ability to repurchase in the future.

Investment Highlights

Improved profitability drives valuation support, but short-term cash flow pressure needs attention

PayPal Q2 EPS $1.40, +29.6% YoY, with non-GAAP operating income of over $1.6bn, up 13% YoY, demonstrating the effectiveness of cost control and profitability optimization.Trading profit rose 7% year-on-year to $3.84 billion, supporting the full-year guidance increase (EPS $5.15-$5.30, +11-14%).However, adjusted free cash flow was only $656m, plunging 53% q-o-q from Q1 and well below expectations of $1.4bn, likely dragged down by a q-o-q increase in opex ($6.78bn vs $6.26bn in Q1) and restructuring costs.In the short term, cash flow pressures could weigh on valuations, but a recovery after Q3 (guiding for $600-700 million for the full year) is expected to ease market concerns

Venmo and BNPL businesses are growth engines, reinforcing platformization strategy.

Venmo's revenue grew >20% YoY and TPV grew 12%, with "Pay with Venmo" payment volume increasing >45%, demonstrating its increased penetration in the consumer payment market, while BNPL business transaction volume grew >20% and monthly active users increased 18%, indicating strong demand for installment payments.Strong demand for installment payments.The company launched "PayPal World" and "Pay with Crypto" which supports >100 cryptocurrencies, targeting 650 million crypto users globally and strengthening the platform layout.The strong performance of Venmo and BNPL may provide a positive catalyst for valuation repricing, especially in light of the expected recovery of e-commerce.

Macro environment and increased competition pose downside risks, need to be wary of the impact of consumer weakness

CEO Alex Chriss pointed out that the slowdown in U.S. retail spending, unstable macro-environment and intensified competition are the main risks. 6% TPV growth in Q2 exceeded expectations but was lower than historical highs, reflecting the slowdown in e-commerce volume growth (only 3% in Q1). 6% TPV growth in Q2 exceeded expectations but was lower than historical highs, reflecting a slowdown in e-commerce volume growth (only 3% in Q1).(Branded Checkout).TPV growth could come under further pressure if consumer demand continues to weaken, with Q3 performance in focus (guidance for TPV implied 4% growth)

AI and global expansion potential open up long term growth, valuation repricing boundaries widen

Management emphasized that AI, advertising and cryptocurrency will reshape the business model, and the CEO said that the next 5 years will see more changes in shopping styles than in the last 20 years.PayPal World is scheduled to go live in the fall of 2025, with the goal of realizing global wallet interoperability, or to increase the penetration rate of the international market (the international share of the current TPV is about 40%).These strategic directions, or for the valuation to provide long-term support, the current P / E 17.36x (LTM) relative to the industry pivot is low, if the market is expected to shift to growth, valuation repricing space can be expected.

Market expectations change free cash flow and guidelines deviation into focus, industry competition pattern has not changed

Previous market concerns include slowing user growth (Q2 active accounts +2%), gross margin pressure and increased competition.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Mortimer Arthur·2025-07-30I bought some yesterday after seeing the ER and the price drop. Hoping this will pump back up.LikeReport

- Valerie Archibald·2025-07-30Added on the tip yesterday, let's go, this is crazy under 100.LikeReport

- AndreaClarissa·2025-07-30Wow, great insights on PayPal's performance! [Wow]LikeReport