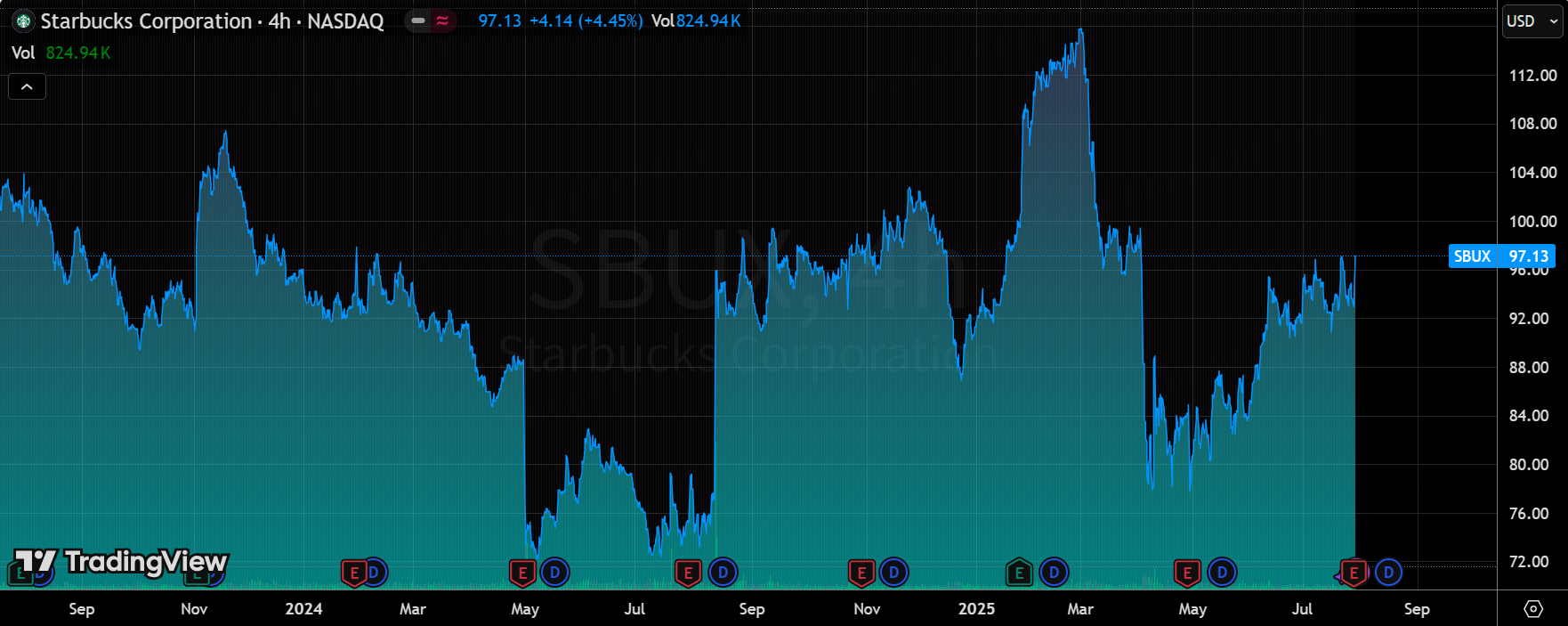

Starbucks Q3 Shock: Profit Crashes 46% But Stock Soars 4%

$Starbucks(SBUX)$ Q3 2025 results show revenue growth of 4.4%, but margins under pressure, with the core challenges being continued same-store sales declines in North America and rising costs.Investors are optimistic about long-term growth potential (+4% after-hours) as transformation program "Back to Starbucks" begins to bear fruit, highlighted by recovery in China.Valuation re-pricing is key to same-store sales recovery and margin improvement in the coming quarters, and focus on the impact of reforms and cost control in 2026.

Core Performance and Market Feedback

Revenue performance: Starbucks achieved revenue of $9.5B ($9.5B) in Q3 2025 (ended June 30), up 4.4% YoY and ahead of the market's estimate of $9.31B ($9.31B), indicating that growth was driven by new-store expansions and menu innovations, but pressure on same-store sales remained.

EPS performance: Adjusted EPS of $0.50 ($0.50) was below market expectations of $0.65 ($0.65) and down significantly from $0.93 ($0.93) last year, with $0.11 of non-recurring costs (e.g., Leadership Experience 2025 investment and taxes) dragging the company down.Same Store Sales: Global same store sales were down significantly.

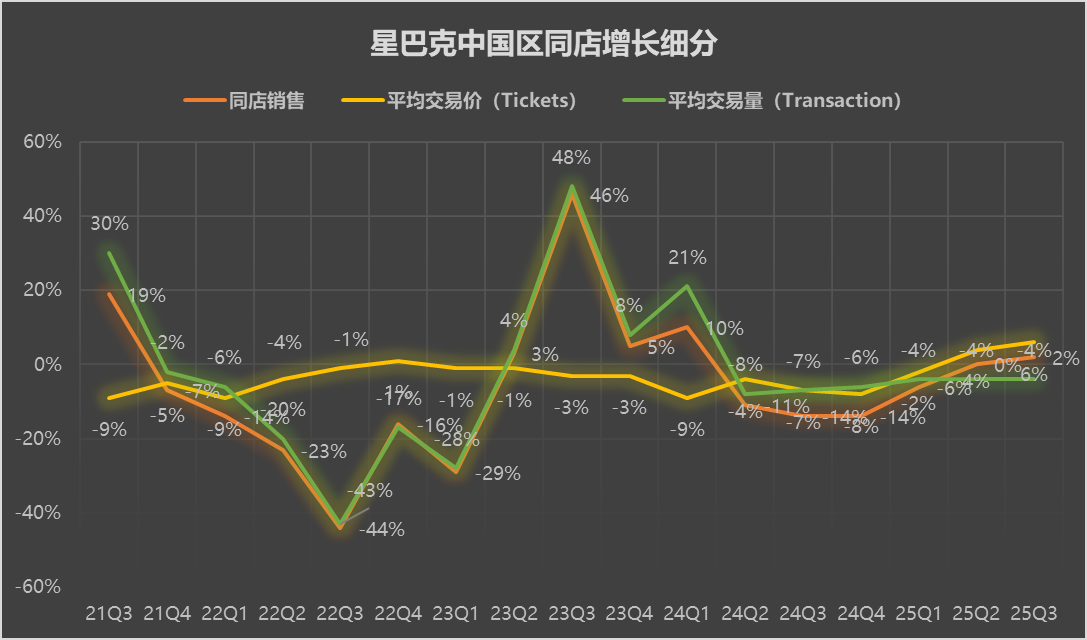

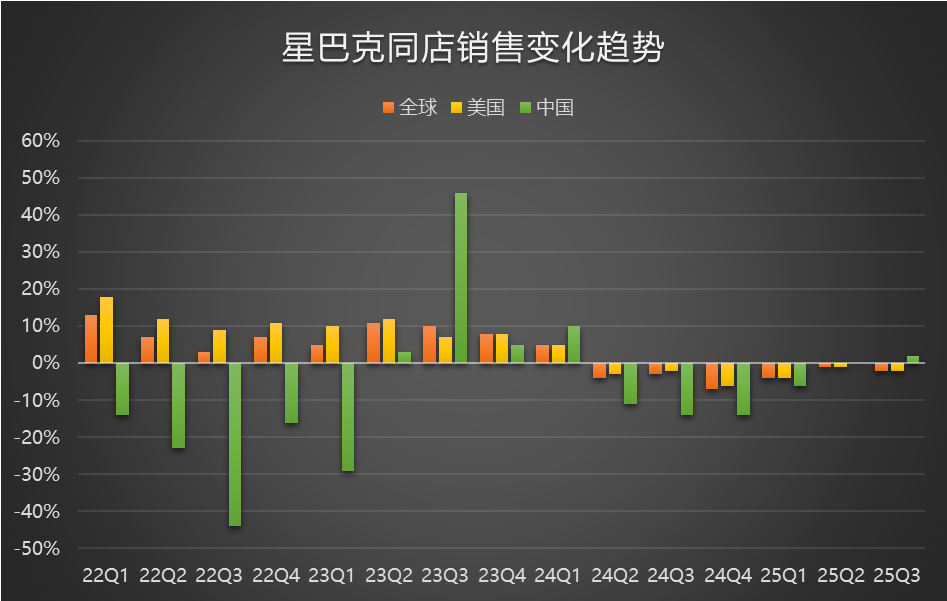

Same-store sales: Global same-store sales declined 2%, lower than the expected -1.3%; North America declined 2%, better than the expected -2.5%; China was a bright spot, up 2% year-on-year, the first positive growth in 1.5 years.

Segmental analysis: North America had the highest revenue share, but same-store sales declined sequentially, reflecting increased sensitivity of U.S. consumers to high-priced coffee and intensified competition (e.g., local chains and discount brands).The Chinese market performed well, with transaction volume up 6%, indicating that the economic recovery and localization strategy (e.g., menu adjustments) are beginning to bear fruit and may become a growth engine in the future.

After the release of the earnings report (after-hours on July 29), the stock price rose 4.28% in after-hours trading against the trend, the market will focus more on the progress of strategic transformation and the long-term signals released by China's recovery, rather than short-term earnings fluctuations, also shows that investors are more inclined to give valuation patience to the "structural transformation period" companies.

Investment highlights

Revenue growth drivers and same-store sales divergence

Revenue of US$9.5bn was up 4.4% YoY, driven by new store expansion (especially in international markets) and menu innovation, but global same-store sales declined 2% indicating pressure on existing store traffic.Same-store sales in North America declined 2%, reflecting weak consumer demand in the US, likely driven by inflation and increased competition, while same-store sales in China were +2%, with transaction volume up 6% for the first time in 1.5 years, indicating that the localization strategy is beginning to pay off.This indicates that Starbucks' growth logic is tilting from stock optimization to incremental expansion. Valuation repricing may be supported by China's market recovery, but continued pressure in North America may suppress short-term expectations.

Adjusted EPS declined to $0.50 from $0.93, while net income fell to $558.3 million from $1.05 billion, pressuring both gross and operating margins.Reasons included $500 million in labor investments (to improve service quality) and $0.11 in non-recurring costs (e.g., "Leadership Experience 2025").These costs are at the heart of the "Back to Starbucks" program, which aims to revitalize the brand by improving the customer experience, but are compressing margins in the short term, which could raise concerns about earnings sustainability.The key to valuation repricing will be the effectiveness of cost control and the speed of margin recovery in the coming quarters.

"Back to Starbucks" Program Begins to Pay Off, North American Reforms Drive Operational Efficiency

Management emphasized that the "Back to Starbucks" program is progressing well, with a focus on artisanal beverages, cozy cafes and personalized service, especially in China, where positive feedback (same-store sales growth) is a source of confidence.The program also includes digital transformation and menu simplification to improve customer engagement.

In the North American market, a number of reforms have been launched around store efficiency and employee management, with the key program "Green Apron Service" (Green Apron Service) having completed the rollout of directly-managed stores across the U.S. in mid-August, with pilot data showing significant improvements in transaction volume and service speed, especially during peak hours, when the efficiency of order processing is particularly improved.especially during peak hours.At the system level, the SmartQ order scheduling system and store management optimization have formed a closed loop, helping to reduce queuing and waiting time, thus improving customer experience.

On the other hand, the Company has implemented cost reduction measures on the store construction side, and has successfully compressed the cost of new store construction by approximately 30%, while optimizing the promotion path for assistant store managers to enhance talent retention and alleviate the pressure on long-term labor costs.However, the additional US$500 million manpower investment spending still exerted significant pressure on margins, especially against the backdrop that transaction volumes have yet to pick up significantly.Despite the recovery in non-member trading, the overall downward trend has yet to be reversed, suggesting that the effectiveness of the reforms will take time to be proven and is not expected to be reflected in an earnings recovery until at least 2026.

Changing Market Expectations and Competitive Landscape

Previous analysts' concerns included the decline in same-store sales in North America, the recovery in China and the ability to control costs.The positive growth in China responded to market expectations in the earnings report, but North America has yet to see significant improvement and cost increases have not been fully hedged.Increased competition in the industry (e.g., local coffee chains and discount brands) may continue to impact Starbucks' pricing power, and the boundaries of valuation repricing may depend on the ability to widen the gap with competitors through digitization and innovation.

Market Focus Tracking (Sell-side Perspective)

Previously, the market focused on: same-store sales decline in North America, recovery in China, cost control ability and digital transformation effect

Earnings report showed +2% same-store sales in China responded to market expectations and showed signs of recovery, but North America has yet to improve, cost increases (e.g., labor investment) weighed on margins, and the effects of digital transformation are yet to be seen (e.g., app user growth data not disclosed).

The 4% after-hours share price gain shows investor recognition of the transformation program, but the P/E multiple of 33.5x (above the industry median of 20.6) suggests that the valuation premium is dependent on future execution.If same-store sales continue to grow negatively, the market may revise expectations downward; conversely, a recovery in China and improved margins could further support valuations.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- JimmyHua·2025-07-30What do you think about SBUX competitors like Luckin Coffee?LikeReport

- Enid Bertha·2025-07-30Heading to 80 level most likely long termLikeReport

- BillyWilliams·2025-07-30Wow, love the transformation journey! [Love]LikeReport

- Valerie Archibald·2025-07-30holding above 90 - still good!LikeReport

- LeoIII.·2025-07-30Interesting takeLikeReport