June CPI Preview: The Cure for Rate Cuts or A Trap for "Soft Landing"?

Abstract

The June inflation report is far from routine - it is a key test of the timing of the Fed's policy shift and a litmus test of the market's belief in the "soft landing" narrative.The performance of core commodities under the shadow of tariffs and the degree of intransigence of housing inflation are two "time bombs" that will directly determine market sentiment and the Fed's path of action.The forward-looking view is exceptionally clear - unless CPI comes in significantly lower than expected (which is relatively unlikely), market bets on a September rate cut look overly optimistic.

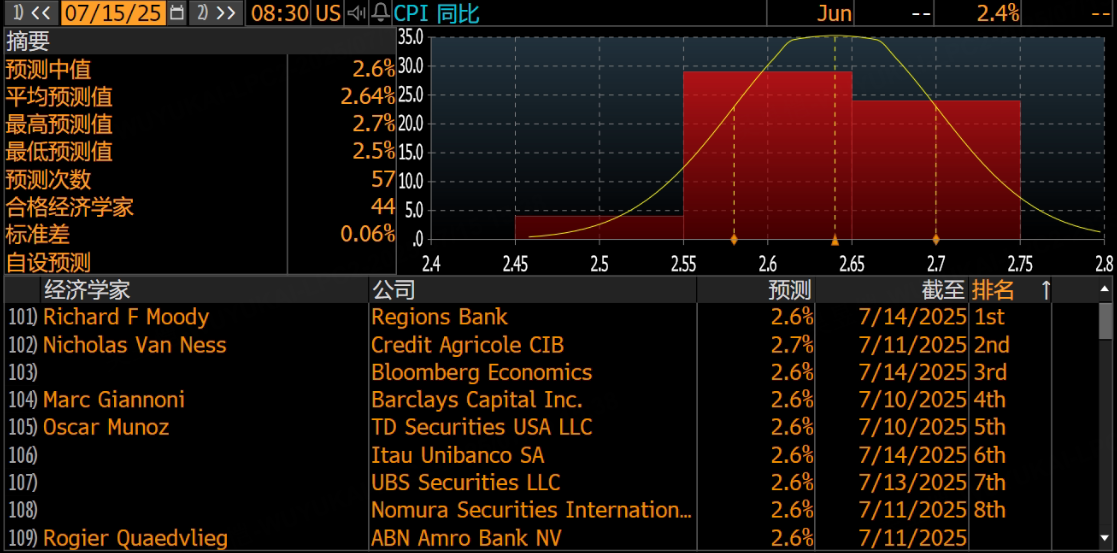

Data Outlook: June Inflation Expected to Slow Across the Board

Based on a combination of high-frequency data, commodity price trends and rental indicators, the current market consensus is cold and unanimous: CPI is expected to slow to 2.6% year-on-year in June, and both headline and core CPI are expected to rise by 0.3% YoY, with the core rising by only 0.1% in May .rose just 0.1% in May.Expectations for the annualized increase in core CPI were compressed into a narrow range of 2.8% to 3.1%.

It will most likely be the key pronouncement on whether the Fed pulls the trigger on a rate cut in September.

Tariff sword sheathed, core commodities under pressure: The tariffs that have been imposed over the past few months are far from a bluff.There are signs that they are actually translating into a tightening of U.S. consumer purchasing power.Core goods CPI is under sustained upward pressure as manufacturers and retailers begin to pass on additional costs to the end-user.This potential variable is an undercurrent that could significantly alter the monthly inflation picture.

Housing inflation "iron ceiling": Despite the seemingly slower pace of rental growth, the housing subcomponent is still widely viewed as the biggest driver of the core CPI uptick.Its stubborn stickiness is the Achilles' heel of any real cooling of inflation, and is unlikely to subside quickly.

Transportation Prices in the Dark: Details of the report further expose the price divide - the used car market is bucking the trend of cooling under dealer incentives, becoming one of the few downward forces;Auto insurance prices maintained a modest uptrend, while airfares showed worrisome signs of recovery, with subsequent volatility remaining a two-way risk, adding uncertainty to the overall data.

Structural analysis: core inflation remains stubborn

Despite the softening data, the structural aspects of inflation have not yet been fully resolved.

Service inflation is sticky: in particular, "non-housing core services" (Supercore), such as transportation, recreational services, insurance, etc., have continued to grow at a monthly rate of more than 0.4%.

Wage push is still going on: Although the labor market is "cooling at the margins", the unemployment rate is still historically low, and wage growth is still supporting service inflation.

In other words, the fall in inflation is "phased", not "final".The Fed saw not a fire was extinguished, but the temperature slightly reduced hearth.

The market and the Fed's expectations of the game

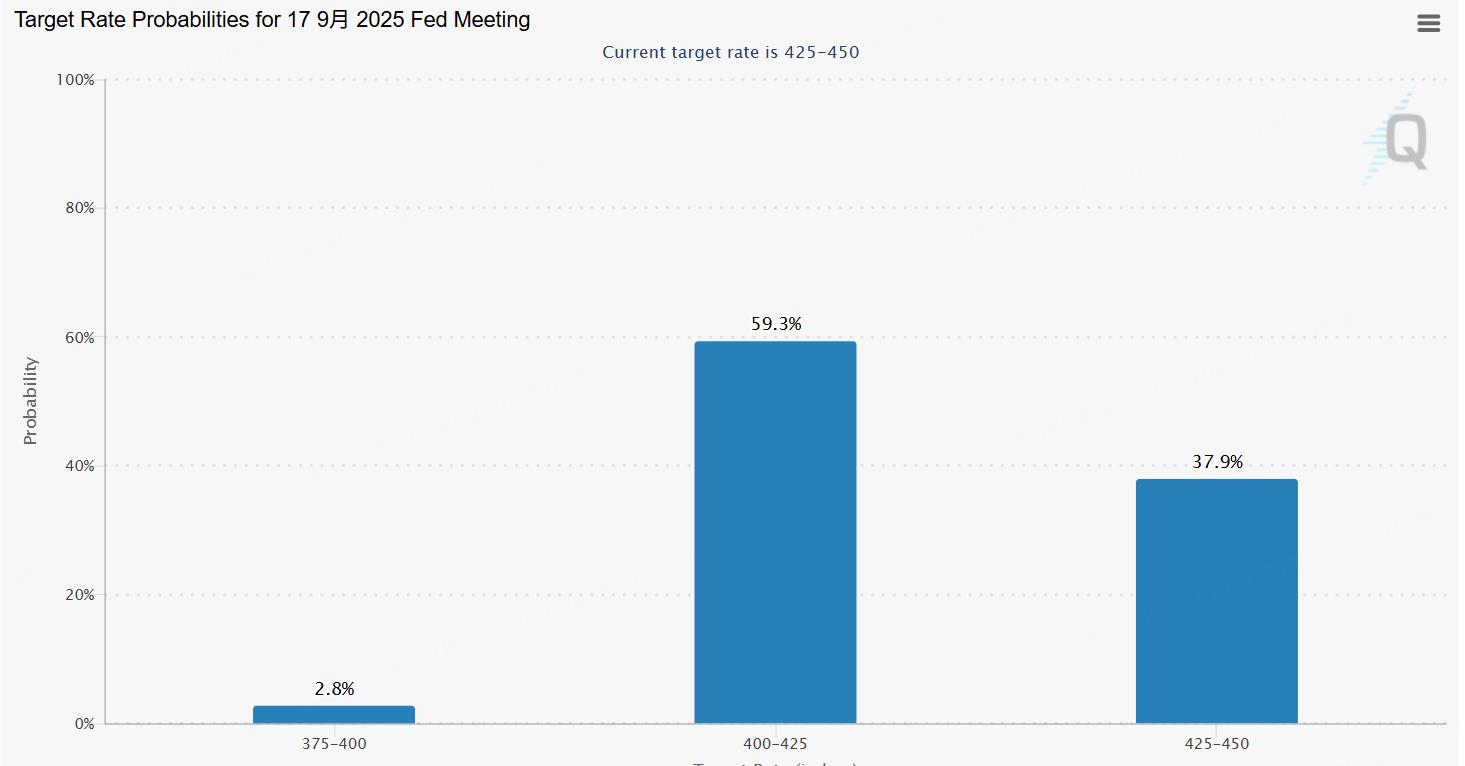

The market has "first bet": the swap market shows that the probability of a rate cut in September is only 59.3%, and even do not rule out two rate cuts within the year.But the Fed has not yet formed a unified voice.

Representatives of the doves (such as Waller) said to see inflation fall can be considered for action; hawks are still cautious, worried that premature relaxation will again trigger the risk of stagflation; CPI data must form a "trend" rather than "isolated cases" in order to promote the policy shift.

June CPI data for the Fed rate cut window prying, can be said to "pull one hair and move the whole body":

If the data is in line with expectations or weaker than expected (e.g., +0.3% MoM or lower): this scenario will be regarded as evidence of the continuation of the "pseudo-cooling" of inflationary pressures, and the market will rekindle its bets!The probability of an impulse rally in risk assets is high as the Fed makes its first cut in September.

If the data unexpectedly hot (such as the core chain rate exceeded 0.3%): this is tantamount to announcing that the "siren wind" of inflation, especially if it stems from the stalemate of housing costs orThe tariff shock would be significant.The Fed will then have no choice but to maintain its high-pressure stance, the hawkish signals of the July FOMC meeting may make a comeback, and the expectation of a rate cut in September will quickly evaporate, and the market may experience a round of painful adjustments.

The deeper concern is that the market's over-obsession with single-month data has obscured structural risks.A spike in energy prices due to geopolitical turmoil, a lack of moderation in wage growth pressures, or a stronger-than-expected pass-through of the aforementioned tariffs in the commodities sector are all well within the realm of possibility to ignite a new price spiral.Even if the June data squeaks out to be moderate, it by no means signals a final victory in the battle against inflation.

Don't just focus on the year-on-year, the real change in the path is the "structural inflection point".

The core of the current round of inflation path is not the "total index" fluctuations, but "structural inflation" reversal. June CPI will become a turning point, but if the service inflation does not cooperate with the fall, the Fed is still difficult to make a decision.We believe that the "structural data + employment indicators" is the decision to cut rates of the two keys, CPI is only one of them.

$iShares 20+ Year Treasury Bond ETF(TLT)$

$US20Y(US20Y.BOND)$ $US30Y(US30Y.BOND)$ $US10Y(US10Y.BOND)$ $iShares TIPS Bond ETF(TIP)$ $SPDR S&P 500 ETF Trust(SPY)$ $S&P 500(.SPX)$ $ProShares UltraPro QQQ(TQQQ)$ $ProShares UltraPro Short QQQ(SQQQ)$ $NASDAQ(.IXIC)$ $Invesco QQQ(QQQ)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- JoyceTobias·2025-07-15The volatility in CPI predictions is concerning.LikeReport

- kookz·2025-07-15Interesting analysisLikeReport