U.S. lawmakers appear to be on the cusp of passing a massive and long-awaitedinfrastructure-investment bill, totaling some $1 trillion.

The legislation should be a boost to businesses likeVulcan Materials(ticker: VMC) andMartin Marietta Materials(MLM), which make concrete and asphalt;Caterpillar(CAT) andTerex(TEX), which make construction equipment; andUnited Rentals(URI), which rents the machinery. Most of their stocks have already jumped on theprospect of infrastructure spending.

But one infrastructure play has been overlooked:Atlas Technical Consultants(ATCX) provides engineering and design services, inspection and certification of buildings and public works, and other construction-related services. More construction means more plans and designs for Atlas to review. These eventually become finished projects that need annual inspections, paying dividends for years.

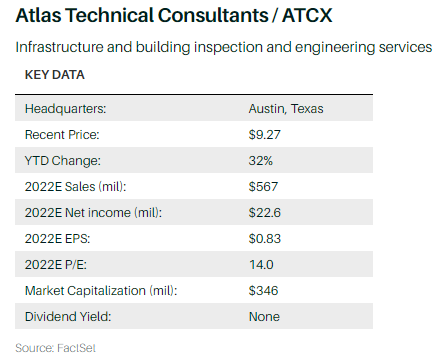

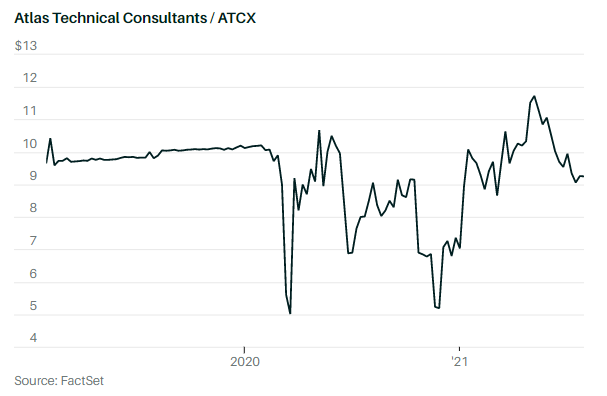

And yet Atlas shares have stalled. At a recent $9, the stock trades for just eight times enterprise value to estimated 2022 earnings before interest, taxes, depreciation, and amortization, or Ebitda. That multiple is a significant discount to companies in related inspection businesses, such asMontrose Environmental Group(MEG) andTetra Tech(TTEK), which trade for more than 22 times EV/2022 Ebitda.

And Atlas has substantial opportunities for growth. Beyond the infrastructure-bill boost, Atlas has a long-term strategy of consolidating the fragmented U.S. inspection-services market while reducing its debt levels. Both should increase its appeal to investors and earn it a higher valuation multiple.

The Austin, Texas–headquartered company went public inearly 2020via a merger with a special-purpose acquisition company, or SPAC. The deal saddled the company with a convoluted capital structure, including multiple share classes, outstanding warrants, and other complications. That complexity has probably kept some investors away, as has Atlas’ relatively high debt load, which comes to 5.5 times net debt to 2021 Ebitda.

Atlas has reduced that complexity—redeeming its preferred equity, buying out warrants, and increasing the stock’s publicly traded float—and is focused on bringing its net debt below three times Ebitda.

Atlas is forecast to grow sales 13% this year, to $530 million, with Ebitda up 21%, to $76 million.

Its customers include state departments of transportation, private building owners, electric and water utilities, airports, schools, hospitals, and more. Its national presence and leading scale helps win and retain marquee projects and big clients, including the U.S. Postal Service, the Environmental Protection Agency, the New York City Housing Authority, Stanford University,Walmart(WMT), andApple(AAPL).

Atlas earned $64 million in adjusted Ebitda over the past four reported quarters, while it had a net loss of $18 million. As of the end of the first quarter, the company had a backlog of $689 million, or more than 140% of its last 12 months’ revenue of $482 million. “I’ve been in this business for 30 years, and it’s by far the highest I’ve seen,” Atlas CEO Joe Boyer tellsBarron’s.

About 70% of the company’s revenue comes from work on existing buildings, pipes, roads, and bridges. Those jobs are nondiscretionary: As we’ve tragically learned at times, infrastructure needs to be inspected and brought up to code at regular intervals, no matter what the economic or pandemic situation is.

The remaining 30% of Atlas’ sales are tied to new construction, which dipped during the pandemic but is nearly back to pre-Covid-19 levels, according to Boyer.

A long-term trend toward outsourcing services by cities and states, stricter environmental standards, and aging infrastructure in the U.S. have been drivers of Atlas’ organic growth in recent years.

That trend has been responsible for about half of Atlas’ 20% compound annual growth in sales since 2016, when it was owned by private-equity firm Bernhard Capital Partners. The other avenue for growth has been Atlas’ acquisition strategy.

“The idea is to find a company in a geography or a service that we don’t dominate in, bring it onto our platform, and cross-sell across our network,” Boyer says.

Atlas’ sweet spot for acquisition targets is about $5 million to $20 million in Ebitda, The company typically pays four to six times Ebitda in a mix of cash and stock. That makes each deal immediately accretive to earnings.

As a small and relatively young public company, Atlas gets minimal coverage from Wall Street, but the three analysts who cover the firm are bullish. “We think the company is in end markets that are strong or recovering; they’ve been winning large contracts, and its backlog has been growing,” says Stifel analyst Noelle Dilts. “So, we feel good about the fundamental revenue outlook.”

She rates Atlas a Buy, with a $14.50 price target, or 11 times her estimate of 2022 Ebitda, which doesn’t include any upside from a potential infrastructure bill. Using a 15 times Ebitda multiple, Sterling’s Silverman sees shares going to $43 three years from now, as debt paydown continues and earnings rise.

Atlas’ balance sheet remains a fixer-upper, but the company has the right foundation.