Summary

- Shares of Uber extended YTD losses after reporting Q2 results, owing to a higher-than-expected adjusted EBITDA loss.

- Uber has been raising driver incentives in order to increase available drivers in preparation for the summer's reopening.

- Rideshare bookings have dramatically rebounded, positioning Uber well for recovery.

- Short-term profitability hits should be ignored, given Uber's long-term market opportunity is still dramatically larger than where it stands today.

This year, the share price behavior of certain stocks that are thought to be obvious "reopening plays" has been a bit bizarre, and in no company other than Uber (UBER) is this more evident. Investors have soured on Uber year-to-date, sending the stock down nearly 20%: in spite of very positive reopening news that has lifted Uber's rideshare bookings. Even better, the company is noting that delivery (UberEats) bookings have held strong, indicating that delivery may have become a more permanent fixture of our daily routines that won't fade post-pandemic.

Losses in Uber picked up steam after the company reported Q2 results in early August. Bookings and revenue topped expectations, but Uber has been stepping up driver bonuses in order to be the most available rideshare app amid this summer's reopening. That strategy hurt the company's overall profitability this quarter, but in my view, recovering rider trends are a far more important accomplishment. To me, this is a very buyable dip in Uber.

The bullish thesis in Uber

Investors often have such a short-term focus: Uber's recent dip was all about the losses it incurred in a single quarter, driven by a temporary factor (a step-up in driver incentives). In my view, patient investors should take this opportunity to review the long-term bullish thesis for Uber:

- Huge $13.8 trillion TAM.Mobility and Delivery each carry $5 trillion market opportunities, and nascent Uber Freight is another massive $3.8 trillion market that is heavily underserved and ripe for tech disruption.

- Formidable marketleadership.In most of the markets that Uber operates in, the company has a leading market share, and usually by a substantial margin. The company has selectively exited markets where it lost share to a local incumbent (Grab in Singapore is a good example), so it can focus on turf where it has the advantage.

- The sharing economy is gradually taking precedence over ownership.In 2021, a semiconductor shortage has dramatically increased the price of cars, both used and new. Even before this price shock and pre-pandemic, many consumers were already questioning the wisdom of car ownership over rideshare. Owning a car comes with maintenance costs, insurance costs, and in urban areas, often hefty parking costs. Gradually, I expect car ownership to decline and for rideshare to become the preeminent form of transportation.

- "Other bets"are numerous.Uber Freight is the best example of a new initiative to drive growth, but grocery and package delivery are others as well. Uber's focus on anything involving mobility gives it a massive greenfield market to operate in.

Rideshare's cost spike is temporary; look ahead to adjusted EBITDA profitability by Q4

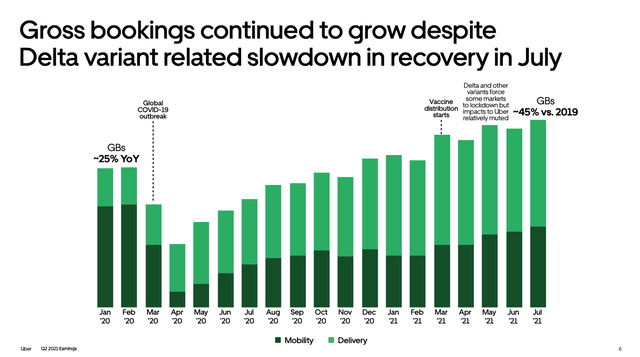

Let's now discuss the biggest issue that plagued sentiment for Uber exiting Q2. The important context to set behind this discussion is that Uber's gross bookings have never been stronger. Gross bookings across both mobility and delivery in July were up 45% versus 2019, having recovered in leaps and bounds from the depths of the pandemic.

Figure 1. Uber gross bookings trends

So it makes sense that Uber wants to invest dramatically to bring drivers back onto the platform and improve availability. Consumers view rideshare as more or less a uniform service: given roughly equivalent prices, a user will likely use the rideshare app that offers the lowest wait times.

As shown in the chart below, the number of drivers on the Uber platform has spiked 50% since February, and over the same time period, wait times have also improved across a number of major urban markets, especially dense urban centers like Miami and Atlanta.

Figure 2. Uber driver and wait time statistics

This is Uber's opportunity to showcase its size advantage over Lyft(NASDAQ:LYFT). If Uber can consistently show better wait times and availability in these markets than its competitors, customers may eventually stop checking competitor applications and rely exclusively on Uber.

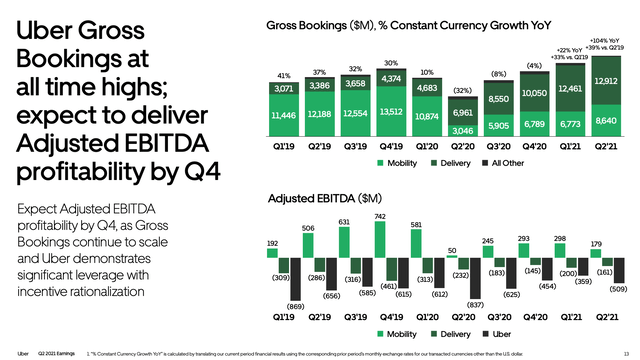

To me, I'm more than happy to sacrifice one or two quarters of adjusted EBITDA profits in order to achieve the right capacity to handle post-reopening rideshare demand. Uber's -$509 million in adjusted EBITDA in Q2 wasn't that bad (it's the best Q2 in two years, in fact, and a slimmer loss even compared to Q2'19 at -$656 million):

Figure 3. Uber adjusted EBITDA trends

The big long-term driver here of course is Delivery's increased economies of scale. The Delivery segment has reached a -$161 million adjusted EBITDA profile, representing a near-breakeven -8.2% adjusted EBITDA margin in Q2: which is substantially improved versus a -$232 million loss (-26.2% margin) in the year-ago Q2.

Uber also notes that its Uber Pass program, a $25/month membership that gives riders a 10-15% discount on rides, no delivery fees, and a 5% discount on restaurant orders, has been picking up steam and now represents about a third of its delivery customers. The increase in frequent ridership driven by this program will also help Uber to scale all of its lines of business. Per CEO Dara Khosrowshahi's prepared remarks on the Q2 earnings call:

Just a year ago we began to roll out Uber Pass in earnest. It now drives 30% of Delivery GBs in the US, and roughly 25% globally. Consumers who regularly engage with both Mobility and Delivery now account for nearly half of our total company Gross Bookings. For these consumers in particular, Pass is a no-brainer, and we see a long runway for increased adoption. We're also seeing the benefits of cross-platform synergies for merchants and other businesses. Uber remains the largest global on-demand delivery platform outside of China, with more than 750,000 monthly active merchants on our platform. And our leadership position continues to grow. We are now the category leader in 8 of our top 10 Delivery markets, with clear number two positions in the US and UK."

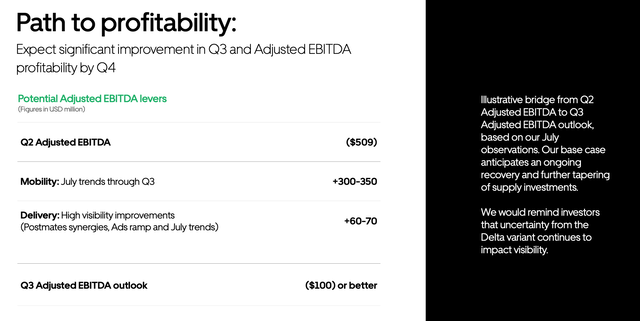

Uber is expecting adjusted EBITDA losses to slim down to "$100 million or better" by Q3, as shown in the chart below:

Figure 4. Uber forward-looking adjusted EBITDA guidance

The improvement will be driven by both continued synergies/economies of scale on the delivery side, plus a slowdown in driver incentives (the company has already achieved tremendous growth in its driver base, and so the driver stimulus it implemented in Q2 will gradually phase out).

Even better, Uber expects to hit consolidated profitability on an adjusted EBITDA basis by Q4, which is what the company originally committed at the start of the year: to reach adjusted EBITDA profitability at a quarterly level at least by the end of 2021.

Key takeaways

Uber has become one of the most globally-recognized consumer brands, and it's one that is emerging from the pandemic as a stronger company. A dramatically expanded delivery business and delivery margins, a strong recovery in rideshare bookings, and new growth opportunities in grocery and freight are just a few reasons investors should retain their confidence in Uber. Buy the dip here.