Why I’m Using an Options Strategy to Lightly Bet on a Modest Pullback?

At present, global risk appetite across risk assets is still mainly driven by U.S. equities. As the marginal impact of Federal Reserve commentary has faded, the absolute dominant force shaping market sentiment remains the progress of the U.S.-Iran war.

$标普500(.SPX)$ $标普500ETF(SPY)$ $SP500指数主连 2606(ESmain)$ $微型SP500指数主连 2606(MESmain)$ $微型SP500指数2606(MES2606)$

Why do we say the Fed’s commentary has become less influential at the margin? The reason is simple. First, there is no certainty that the so-called new chair, Warsh, will actually be able to take office smoothly. Second, even if he does take office, the current environment still does not allow the Fed to make a clear and targeted interest-rate decision. Internal divisions within the Fed are also widening, and Warsh’s remarks have been inconsistent, with his stance shifting back and forth. The most likely outcome is that as long as the war continues, the Fed will keep rates unchanged. Beyond that, there is still no visible policy path with any real directional clarity, so the market is pricing Fed rhetoric less and less.

$纳指100ETF(QQQ)$ $纳斯达克(.IXIC)$ $NQ100指数主连 2606(NQmain)$ $微型NQ100指数主连 2606(MNQmain)$

If Fed commentary no longer deserves too much attention, and if the drawn-out pattern of fighting while talking between the U.S. and Iran still cannot be resolved in the short term, then the market will naturally fall into a phase of sharp consolidation at elevated levels. That is because, based on current conditions, both the upside and downside in U.S. equities appear constrained.

$道琼斯指数主连 2606(YMmain)$ $微型道琼斯指数主连 2606(MYMmain)$ $道琼斯(.DJI)$ $微型道琼斯指数2606(MYM2606)$ $道琼斯ETF(DIA)$

Let us first briefly discuss why the downside in U.S. equities looks limited.

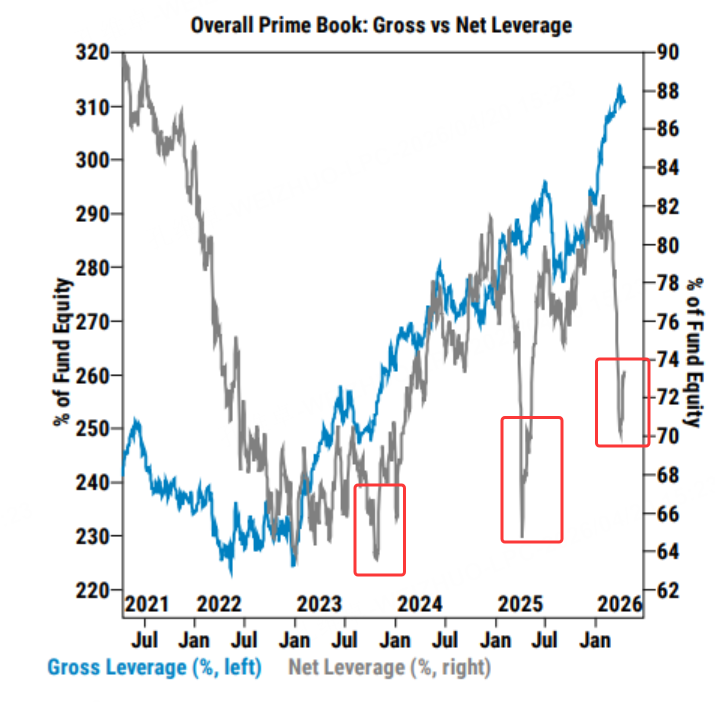

To begin with, asset-management positioning still maintains relatively high exposure to U.S. equity risk, and net leverage has also risen noticeably following the previous rally.

This suggests that institutional capital using leverage—the so-called smart money—added to long U.S. equity positions over the past week, because they believe the worst has already passed.

$SPDR能源指数ETF(XLE)$ $消费品指数ETF-SPDR主要消费品(XLP)$ $消费品指数ETF-SPDR可选消费品(XLY)$

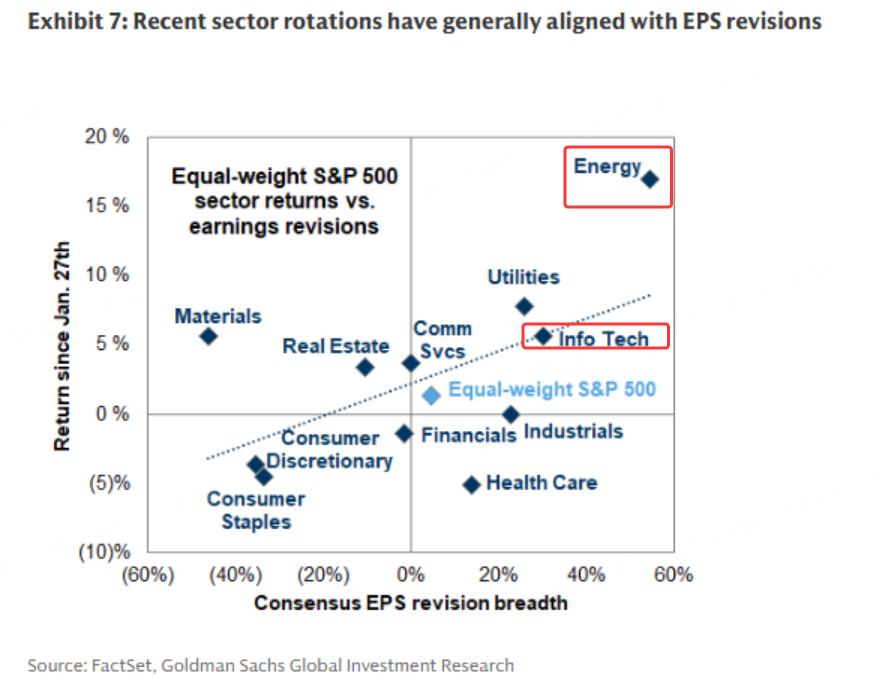

In addition, Goldman Sachs raised its 2027 average earnings forecast for the S&P last week by 3%. Meanwhile, the market’s average price-to-earnings ratio is only 21 times, which is still 5% below the expectation from January 2026. The main drivers behind this upward revision were the energy and IT sectors.

$黄金主连 2606(GCmain)$ $微黄金主连 2606(MGCmain)$ $1盎司黄金主连 2606(1OZmain)$ $黄金ETF-SPDR(GLD)$

The upward revision in earnings has made U.S. equity valuations more stable. Against the backdrop of surging inflation and the risk of oil prices moving out of control, rising yields are now exerting marginally less downward pressure on equities. In other words, U.S. equity indices have developed greater tolerance for higher yields.

$白银主连 2605(SImain)$ $迷你白银主连 2605(QImain)$ $2倍做多白银ETF-ProShares(AGQ)$ $白银ETF-iShares(SLV)$

At the same time, Goldman Sachs data shows that global equity funds have recorded net buying for two consecutive weeks, driven entirely by long-side buying. Europe and emerging Asia led in net inflows. Macro products also saw net buying for a third straight week, again almost entirely driven by long-side demand, while net trading in single stocks remained relatively small. Information technology, communication services, and healthcare posted the largest net buying globally, while consumer goods, industrials, and materials saw the largest net selling.

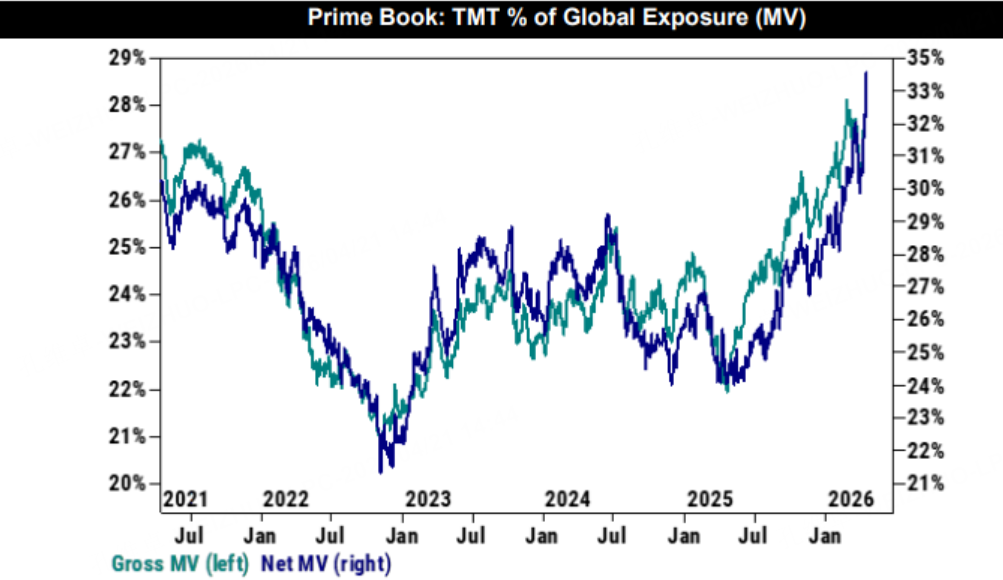

At present, TMT exposure in global equity fund positioning has reached the highest level in history, which suggests that this smart money may no longer believe there is significant downside risk ahead.

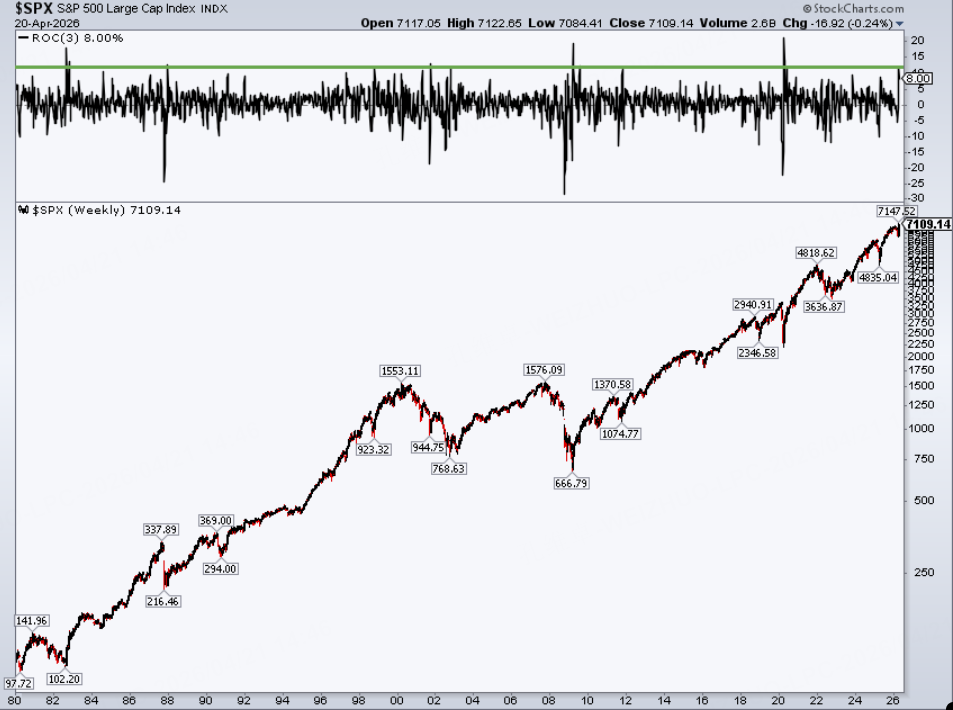

Because CTA funds previously bought aggressively at the lows in U.S. equities, the S&P posted a weekly gain over the past week that ranks 11th largest since 1950. That is already a very significant rally. After a move of that size, we do not believe there is still room for another major leg down. Market sensitivity to the U.S.-Iran war is also gradually declining.

$美国原油ETF(USO)$ $WTI原油主连 2606(CLmain)$ $小原油主连 2606(QMmain)$ $WTI原油2605(CL2605)$

That said, while a deep pullback may be unlikely, a modest correction is still very possible. I have already explained why downside in U.S. equity indices appears limited, so the next question is: why is the upside also limited?

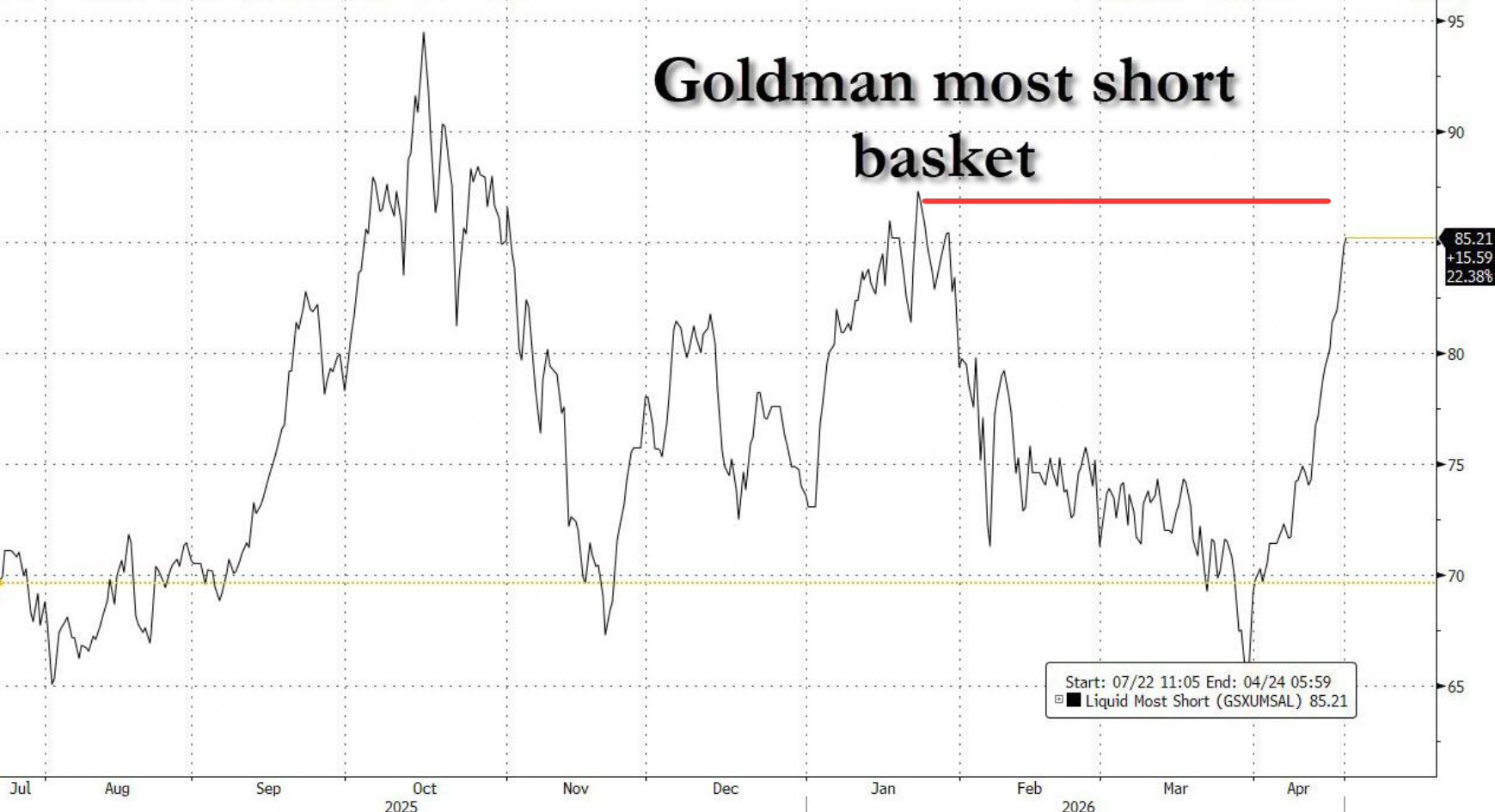

The answer is straightforward. Since U.S.-Iran negotiations have not ended, the possibility of further conflict remains high. For that reason, we cannot assume there is still much room for U.S. equities to break decisively higher. In addition, Goldman Sachs data shows that the rebound in its basket of the most heavily shorted stocks has already nearly returned to the level seen before the U.S.-Iran conflict.

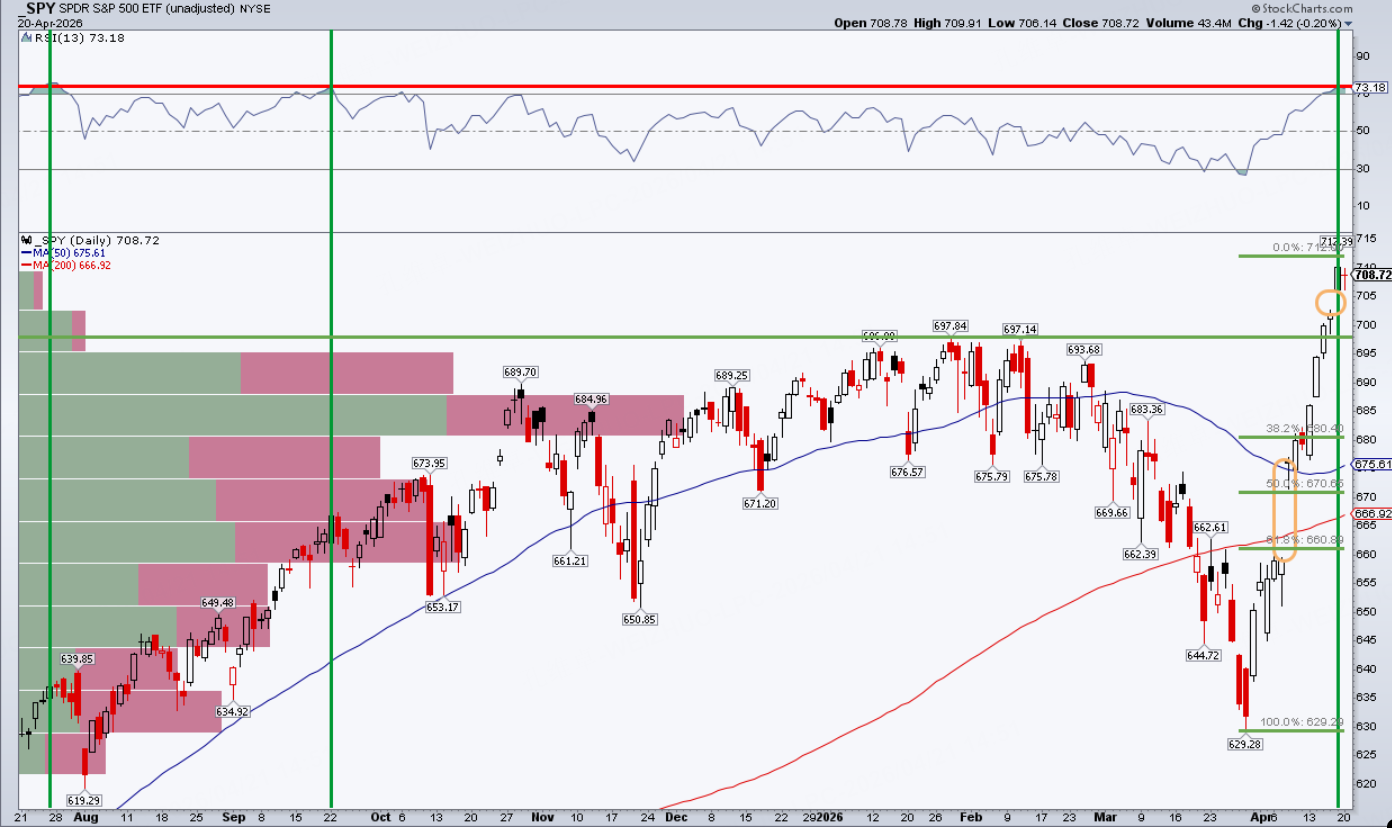

That means that once short covering comes to an end, the probability of a pullback becomes quite high. From a technical-model perspective, the S&P’s overbought reading has already reached the elevated levels seen before previous major corrections. In the absence of any additional bullish catalyst, we have reason to believe that U.S. equities could experience a meaningful pullback from current levels.

So how should we position for a correction in a market where the likely range may not be large, but where prices are fluctuating at elevated levels? I am considering a bearish put spread using options, with SPY as the underlying. The idea would be to buy a near-the-money SPY put at relatively high levels, while simultaneously selling a lower-strike put below the 20-day moving average, in order to build a bear spread structure.

Based on this view, the strategy can generate a profit as long as SPY falls below 701 within the next nine days. The maximum loss is also smaller than the maximum profit, which makes the risk-reward profile relatively attractive. Of course, this is a combination strategy designed for a range-bound market. If SPY rises above 701 nine days from now, the trade will still lose money, so there is definitely risk involved.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- MojoStellar·04-21thank you for sharing your insightful analysisLikeReport