Demand for safe-haven U.S. debt has increased, is it time to go long?

The month-to-date experience seems to suggest that it only takes a wave of typical safe-haven buying to wake up the previously sleeping US Treasury Bond market and push benchmark yields to their lowest point in months...

At a time when the shutdown of the U.S. government caused the key employment and inflation data to be "difficult to produce", the panic caused by regional bank credit risks strongly shook the U.S. Treasury Bond market last week-this round of turmoil coincided with the U.S. bank stock index hitting the biggest drop since the April "Liberation Day" tariff.

As panicked investors flocked to Treasury Bond as a safe haven, the yield on the two-year U.S. Treasury Bond, which is sensitive to interest rate policy, fell below 3.4% last week, hitting a new low since 2022; The 10-year Treasury Bond yield hit its biggest drop since April, falling below 4% in midweek. This is the second influx of safe-haven buying of U.S. bonds this month-the rekindling of trade tensions earlier in the week had triggered a larger rise in U.S. bonds during the session.

Priya Misra, portfolio manager at JPMorgan Investment Management, said,"U.S. debt has become an excellent safe-haven hedging tool in the past week."

Misra pointed out that if there are new credit concerns or trade tensions, yields may decline further. The institution is currently holding 5-to 10-year Treasury Bond, which enables it to "hold promising credit bonds with more peace of mind".

At present, signs of weakness in the U.S. job market have convinced market traders that it is a foregone conclusion that the Federal Reserve will cut interest rates by 25 basis points at the end of this month. In view of the high valuation of stock and credit markets, investors are locking in the 10-year U.S. Treasury bond, which is still as high as 4% for the time being, as an excellent safe-haven option.

Even the 30-year Treasury Bond has risen recently, partially offsetting people's fears of global "currency depreciation trade", although major economies still have huge borrowing needs-this demand has boosted the price of gold to a record of more than $4,000 an ounce.

Ballast stones in times of crisis

Industry insiders pointed out that this month's experience once again reminded people of the traditional role of U.S. debt as the ballast stone of investment portfolios during the crisis. This is also the opposite of what happened in a brief period in April, when reciprocal tariffs introduced by US President Donald Trump roiled the market and raised concerns that global investors would avoid Treasury Bond. For a period of time, U.S. bonds fell along with U.S. stocks and the U.S. dollar.

AndThe sudden rise in bond prices reminds more people of March 2023-when the collapse of Silicon Valley Bank triggered a fall of more than 100 basis points in two-year yields.

Considering the current position of the 10-year U.S. Treasury yield, many bond market traders are also closely focusing on the gains and losses of the 4% mark.

The 10-year U.S. Treasury yield has only fallen below 4% a few times since April. Last week, it once fell to 3.93%, the lowest point since April 7th, and then rebounded above 4% before the close on Friday, as Trump's tone on trade issues softened and the performance of regional banks eased credit concerns.

Judging from bets in the options market, some bond market traders are now using options to prevent the 10-year yield from falling further below 4%.Deeper yield declines could add to bond gains by triggering further hedging-which could add momentum to what looks set to be the best year for the U.S. bond market so far this year since 2020. As of Thursday, the Bloomberg U.S. Treasury Bond Index has gained 6.6% this year.

A team of Morgan Stanley interest rate strategists headed by Matthew Hornbach is one of those who believes that the 10-year U.S. Treasury yield still has room to fall. They wrote in a note this month that investors should "affectionately say goodbye" to the days when the 10-year U.S. Treasury yield was above 4%, partly because of concerns that the longer the government shutdown lasts, the greater its impact.

However, economic data to be released this week may temporarily delay the downward trend of U.S. bond yields.The September CPI originally scheduled to be released on October 15 in the United States has been confirmed to be postponed to this Friday (October 24) due to the government shutdown. Morgan Stanley's Hornbach said investor concerns about the results of the data release "may temporarily prevent the 10-year Treasury Bond yield from falling too much, i.e. well below 4%".

At present, media survey economists generally expect that the month-on-month increase of U.S. core CPI in September will remain unchanged at 0.3%, making the year-on-year increase remain at 3.1%, much higher than the Federal Reserve's 2% inflation target.

"There is room for the 10-year Treasury Bond yield to fall below 4%," said Gregory Faranello, head of U.S. interest rate trading and strategy at AmeriVet Securities. "But things need to get much worse than they are now."

What is a diagonal spread?

diagonal spread refers to the spread established using options with different strike prices and different expiration dates. Generally, the duration of the long leg in the spread is longer than that of the short leg. Diagonal spreads include diagonal bull spreads versus diagonal bear spreads.

The diagonal bull spread is basically similar to the bull subscription spread strategy, except that it has been upgraded and improved again.The difference is that the two options for the diagonal spread have different expirations, the trader buys a longer-term call option with a lower strike price and sells a shorter-term call option with a higher strike price. The number of call options bought and sold is still the same.

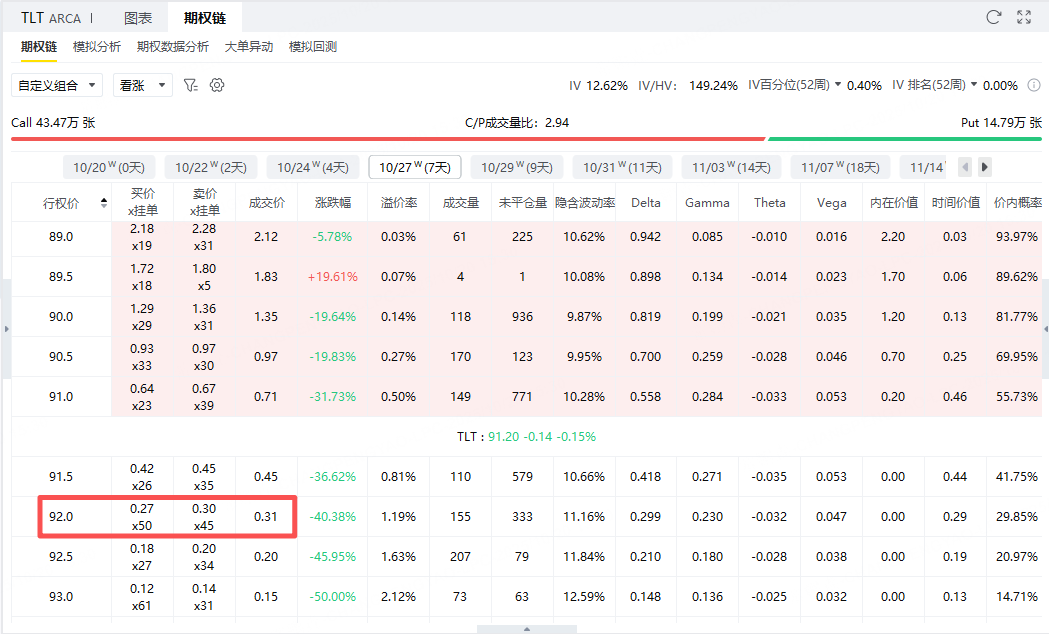

TLT Diagonal Spread Case

Assuming investors are bullish for the next year$20 + + Years US Treasury Bond ETF-iShares (TLT) $, you can directly buy the call option with an exercise price of 90 and an expiration date of August 21, 2026. This option becomes our long leg, which costs $495 at the latest transaction price.

After the long leg is established, we can establish the short leg according to a shorter cycle than the long leg. Here, we can choose to establish it on a weekly basis. Choose to sell a call option with a strike price of $92 and an expiration date of October 27 and get a premium of $31.

Here, if the call option sold is not exercised, it will generate a profit of $31, which is about 6.26% relative to the cost of $495 on the long side. However, the short leg can be executed once a week. When the remaining date of the long leg is as long as 305 days, investors can sell dozens of call options. If some sold call options can successfully obtain premium, it will greatly reduce the cost of buying the call option itself, and even get the call option for free.

Compared with buying bulls alone, the diagonal spread obtains an additional premium income, which reduces the overall net premium expenditure of the strategy, and the break-even point of the strategy is also shifted to the left, and the winning rate is also increased accordingly. AdditionallyThe selling point of the diagonal spread can be controlled by investors themselves, so different short-selling efforts can be selected in different cycles to facilitate investors to control risks. Diagonal spreadEssentially, it is a low-cost call option strategy that is worth investors studying.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.