Low Margin Panic? Oracle's Data Proves AI Training is Just the Start!

$Oracle(ORCL)$ is transforming from a "status quo defender" to a "disruptor" amid the AI wave. Recent media scrutiny over OCI's (Oracle Cloud Infrastructure) low margins and customer concentration has emerged, while the upcoming Financial Analyst Day will serve as a key catalyst.

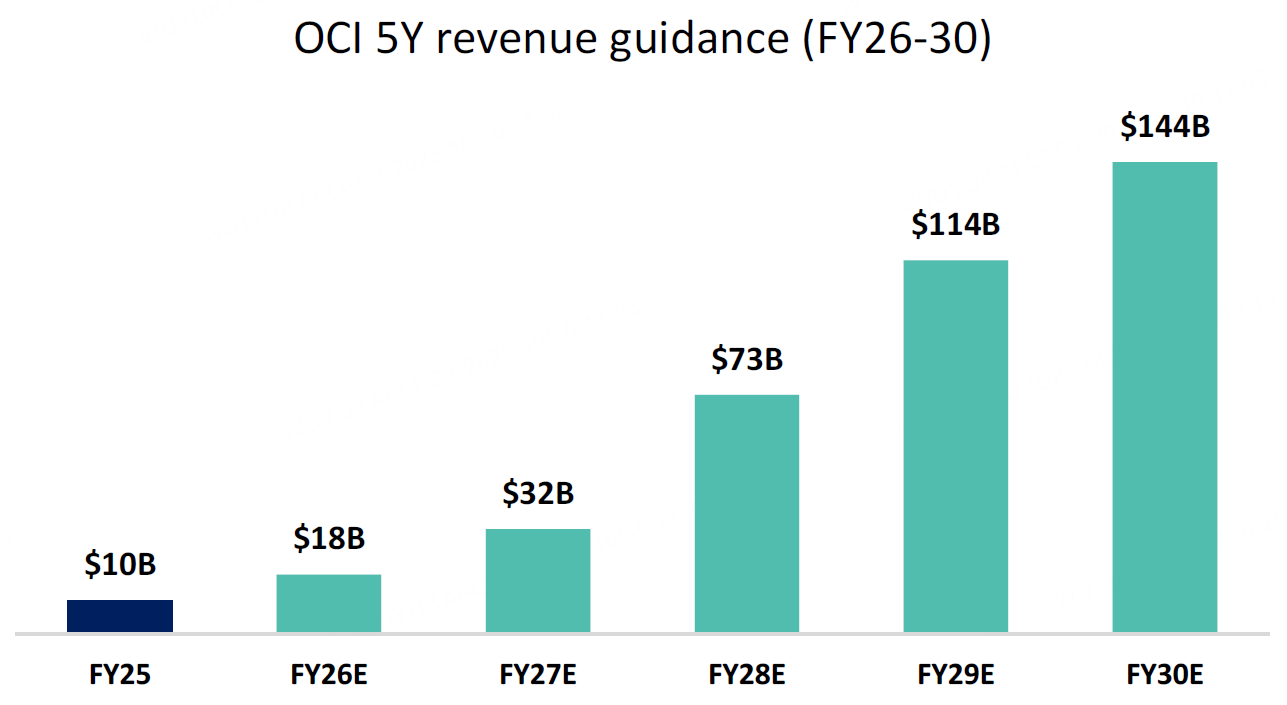

OCI Growth Path: The "Third Pole" Ambition from $10B to $144B

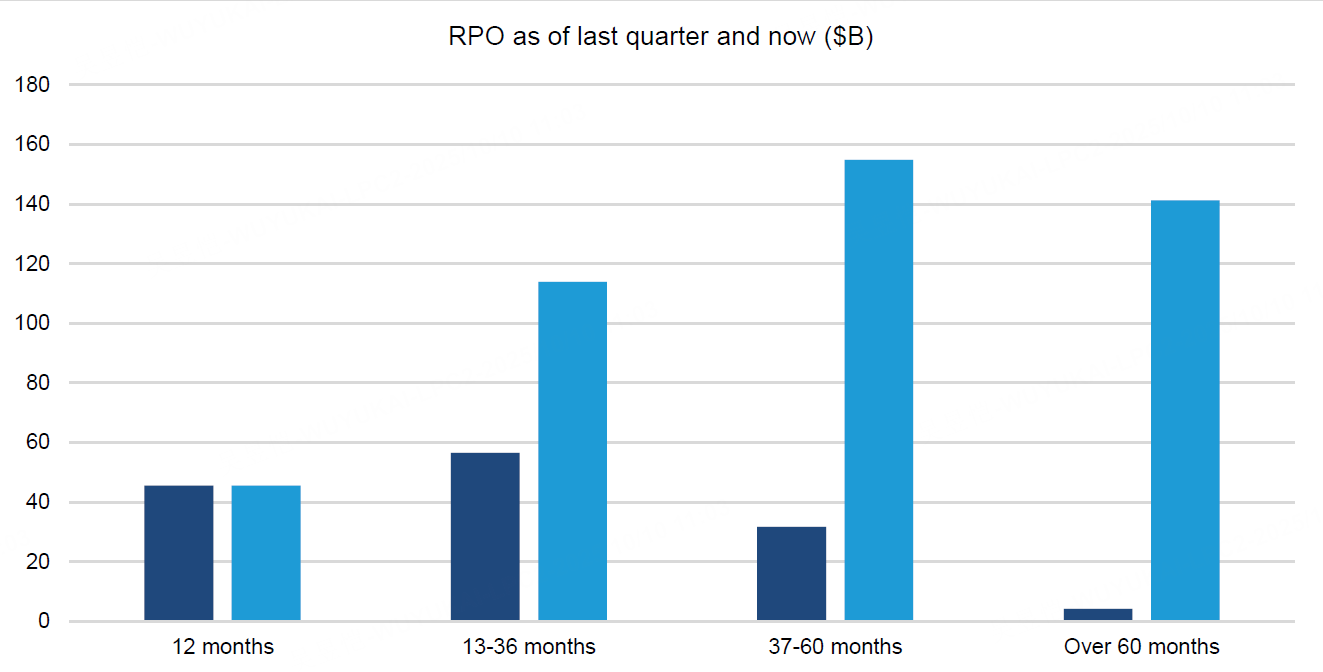

Oracle's cloud business is accelerating its evolution. Over the past year, the company has progressively disclosed multiple large-scale AI contracts since its FY28 long-term guidance in October last year: An August 30th 8-K filing revealed that several major deals will contribute over $30 billion in cloud revenue starting from FY28; The Q1 earnings report on September 9 provided five-year guidance for OCI: $18B in FY26, $32B in FY27, $73B in FY28, $114B in FY29, and $144B in FY30, representing a compound annual growth rate exceeding 70%. RPO (Remaining Performance Obligations) surged $317 billion quarter-over-quarter, with $140 billion to be recognized after five years, highlighting the contracts' extended duration and substantial cash flow potential.

This path is built upon a unique data center architecture and intellectual property. Oracle is targeting the position of the world's largest AI training provider, aiming to become the third-largest hyperscaler by revenue. The key lies in "up-selling": training contracts will drive expansion into inference services and CPU/GPU PaaS, reaching both new and existing customers. This marks Oracle's third business transformation—following ERP/database cloud migration and OCI CPU expansion—with AI becoming the new growth engine.

Financial projections support this optimism: FY25 revenue of $573.99 billion, projected FY26 revenue of $670.39 billion, and FY27 revenue of $850.77 billion, representing a 21.7% CAGR. Adjusted EPS is projected to rise from $6.03 to $8.60 by FY27, a 27.5% increase. While the operating margin slightly decreased from 43.6% to 41.3%, the net profit margin remained stable above 29%, indicating controllable efficiency.

Addressing Market Noise: Low Margins and Customer Concentration Are Not Fatal Flaws

Recent news reports have fueled considerable panic, such as The Information's claim that Oracle's AI sales gross margin is only 10%-20%, averaging 16%; while the WSJ indicated that $300 billion in RPO largely stems from a single OpenAI client. These concerns are exaggerated.

First, low margins stem from the inherent nature of AI training services: they are inherently lower than inference or traditional IaaS/PaaS offerings, yet still offer sufficient profit potential and serve as a gateway. Assuming AI training margins gradually climb from this year's -15% to 25% (referencing CoreWeave's current level), this remains far below Microsoft Azure's early -68% (FY16). However, with scaling and efficiency gains, profitability can rapidly turn positive—Azure reached 32% by FY19. Microsoft's AI business (including Copilot and Azure Inference) also operated at negative margins early on before surging to 30%-40% later. Oracle possesses greater scale and proprietary IP, enabling faster marginal improvements. Additionally, high-margin segments like multi-cloud databases and SaaS will cushion pressure. Assuming an 8% annual OPEX increase (conservative estimate), GAAP operating margins can remain flat, with cumulative FCF reaching $348 billion from FY26 to FY35. However, FY26 to FY29 may see a net negative of $87 billion (peak of facility construction).

Second, customer concentration risk is limited. While OpenAI represents a significant contract (5-year term, approximately $300 billion), it does not account for the entire RPO—the portion beyond five years already exceeds its $115 billion infrastructure spending (through 2029). Cumulative OCI growth (from $10B in FY25 to $114B in FY29) requires multi-source drivers, including other AI training clients and sovereign cloud demand. Microsoft avoided the training business not because it was "bad business," but due to resource allocation (prioritizing inference), Capex concerns, and regulatory worries. Oracle seized this opportunity to fill the void, positioning itself as a participant in the AI revolution rather than a bystander.

Financing is another key focus. Oracle will bridge its Capex gap using a mix of customer prepayments (referencing CoreWeave's 15%-25% TCV), debt, and vendor financing. With short plant construction cycles (only months from cash outlay to launch) combined with prepayments, negative FCF can be compressed by half or more. Management maintains a conservative approach, avoiding dividend adjustments (current yield 0.7%) or aggressive buybacks.

The following are conclusions drawn by Ming-Chi Kuo from his semiconductor industry research, which also debunk the loss claims as a misunderstanding.

Valuation Comparison Enhances Attractiveness: ORCL NTM P/E 42.8x, higher than Salesforce's 20.1x but lower than Snowflake's 183.8x; EV/Sales at 13.7x, with PEG ratio declining to 1.2x (FY27). Aligned with peers like $Adobe(ADBE)$ and $Microsoft(MSFT)$ AI potential is reasonably priced.

FAM Outlook: Cash Flow Details May Unlock Market Confidence

The October 16 FAM is a key milestone. While primarily for investors, it is recommended to review the full Oracle Cloud World agenda. Anticipated highlights include:

Cash Management: Detailed Analysis of the Capex Light Model, Prepayment Mechanism, and Shortened Factory Construction-to-Launch Cycle to Alleviate Free Cash Flow Concerns.

Profit Guidance: Focus not on gross margin details, but on the revenue-driven path to EPS/EBIT growth.

Total Revenue Update: Beyond OCI, overall guidance for FY29/FY30 highlights robust expansion in SaaS and databases.

New contract hints: Potential disclosure of more large orders, reinforcing the multi-client narrative.

Technical Differentiation: Emphasizing the CPU-centric OCI's advantages in sovereign/private cloud environments, and the competitiveness of GPU design for AI training/inference.

If management delivers on these promises, stock price volatility may stabilize—ORCL is up 73.2% year-to-date, far outpacing the S&P 500's 14.8% gain.

Investment Perspective

Oracle is transforming from a cloud laggard into the third major player in AI infrastructure. Its low gross margins represent growing pains rather than structural flaws. Recent noise has amplified uncertainty, but clear guidance following the FAM meeting will catalyze upward momentum. At current prices, the 26% upside potential warrants attention—suitable for medium-to-long-term allocation. Risks include capital expenditure overruns or slowing AI demand; we recommend adding positions on dips.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- SiliconTracker·2025-10-10Wow 70% CAGR is no joke lah! Oracle's cloud game strong1Report

- Merle Ted·2025-10-11Why this dropped harder than any other tech stocks in AHLikeReport

- Mortimer Arthur·2025-10-11Oracle is holding up really well.LikeReport

- GregoryRichardson·2025-10-10Impressive insightsLikeReport