⏰Tick-Tock, Cisco! Only 50% AI Orders Turned Cash... Race Against Time

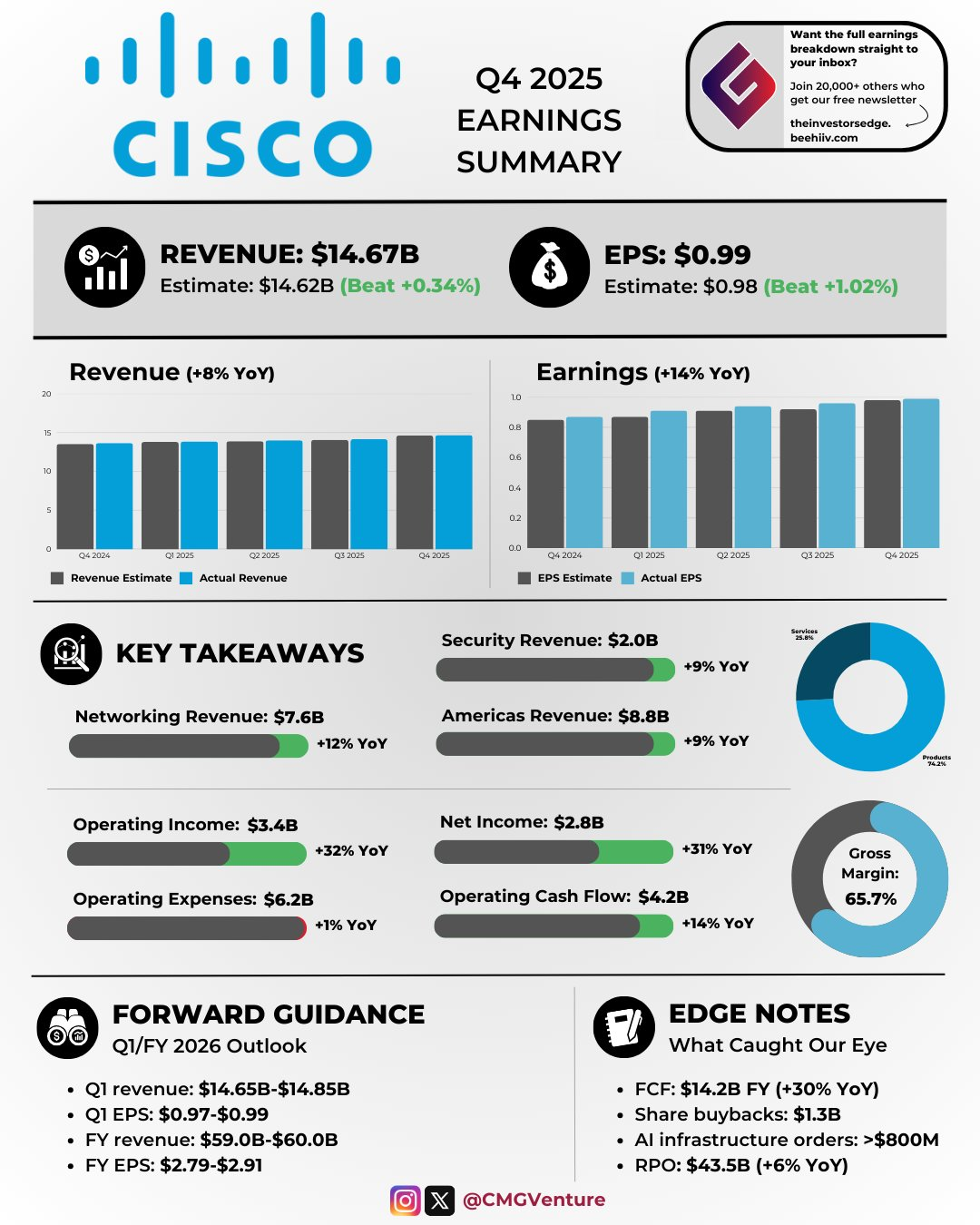

$Cisco(CSCO)$ delivered outstanding performance in the fourth quarter of fiscal year 2025 (calendar year 2025Q2), with key highlights including explosive growth in AI infrastructure orders and profitability exceeding expectations. Quarterly revenue reached $14.7 billion (up 8% year-over-year), with non-GAAP EPS of $0.99 (up 14% year-over-year), both exceeding the upper end of guidance. Annual AI orders exceeded $2 billion (twice the original target), validating its leading position in AI infrastructure. Potential drawbacks include slowing growth in the security business (orders up 9% year-over-year) and weak demand from the public sector (orders down 6%), with a need to monitor the pace of AI adoption in the enterprise sector.

Detailed explanation of key financial data

Revenue of $14.7 billion (up 8% year-over-year, up 4% quarter-over-quarter). Drivers: Explosive demand for AI infrastructure (AI orders exceeded $800 million in Q4), 12% growth in network business (driven by switching/routing/supercomputing centers), offsetting the decline in server business. Above Expectations: Exceeded the upper limit of the guidance range (14.65–14.85 billion), primarily due to a surge in cloud customer orders (four out of the top six supercomputing customers saw growth exceeding 100%). Structural changes: Product revenue share increased to 74% (up 10% year-over-year), with service revenue remaining flat; AI-related systems accounted for two-thirds of orders, and optical modules accounted for one-third.

AI infrastructure orders: Over $2 billion for the year (up 100% year-over-year). Drivers: Expansion of supercomputing customer backend networks (e.g., Nexus switches paired with NVIDIA GPUs), sovereign clouds (e.g., G42 in the Middle East), and new customer expansion (e.g., Humane, Stargate UAE). Above Expectations: Achieved twice the target (1 billion USD), validating Cisco's Silicon One technology advantage. Risk Factors: Enterprise AI orders remain in the early stages (potential orders in the hundreds of millions of USD), with revenue recognition lagging (only 1 billion USD in revenue recognized for the year).

Non-GAAP gross margin: 68.4% (up 50 bps year-over-year). Drivers: Increased proportion of high-margin AI systems, supply chain cost optimization, and growth in software subscription revenue (accounting for 54% of revenue). Above expectations: Reached the upper end of the guidance range (67.5–68.5%), with tariff impacts (30% in China, 25% in Mexico) partially offset by component exemptions. Structural changes: The gross margin of the security business was dragged down by traditional products, but new products (such as HyperShield) achieved a gross margin of over 70%.

Remaining performance obligations (RPO): $43.5 billion (up 6% year-on-year). Drivers: Product RPO up 8% (AI orders dominate), with 50% to be recognized as revenue in the next 12 months. Weaker than expected: Growth slowed from the previous quarter (+7%), reflecting delays in public sector orders. Signals: High short-term revenue visibility, but corporate-side conversion requires monitoring.

Performance guidance and management statements

FY2026 Guidance. Revenue: $59.0–60.0 billion (up 4–6% year-over-year); EPS: $4.00–4.06 (up 5–7% year-over-year). Q1 Guidance: Revenue $14.65–$14.85 billion (year-over-year +6.5%), EPS $0.97–$0.99.

Overall neutral to optimistic. Assuming no changes to tariff policies, public sector demand is expected to recover in H2; AI revenue forecasts remain unchanged. Full-year growth implies acceleration in H2 (sovereign cloud orders to be finalized, park network upgrades to commence), with the CEO stating that "FY2026 will be Cisco's strongest year ever."

Key Investment Points

Structural trends: AI and network upgrades are long-term trends.

Sustainable Growth Areas: 1. AI Infrastructure: Supercomputing center cluster construction (200G/800G switches), enterprise inference endpoint deployment (Nexus+GPU solution). 2. Network Upgrade Cycle: The eight-year replacement cycle for Catalyst 9K switches has begun, with Wi-Fi 7 adoption growing at a triple-digit rate. Short-term risks include fluctuations in tariff exemption policies (potential impact on gross margin if canceled by 2026) and the pace of sovereign cloud order implementation (geopolitical approval delays).

We believe that Cisco's networking and security business is a sustainable long-term growth area, particularly AI infrastructure orders (over $2 billion for the full year) and industrial IoT (double-digit growth for five consecutive quarters). These are driven by structural demand from global digital transformation and AI deployment, showing an accelerating trend compared to previous quarters (e.g., AI orders of only $1 billion in the 2024 fiscal year). In contrast, the collaboration business (growing by only 2%) may be more dependent on short-term trends like remote work sentiment rather than core drivers; the flat performance of the services business reflects market saturation in mature markets, but the 54% increase in subscription revenue may indicate potential for a shift toward platformization.

Valuation Discrepancy: AI Premium Not Fully Priced

The current valuation implies a high growth expectation, with a PEG ratio of approximately 3.26 and a P/E ratio of approximately 17.79, which is higher than that of peers such as Arista (PEG 1.42) and HPE (PEG 1.02). The market may have priced in AI growth but overlooked tariff risks, leading to a slight decline in the stock price after hours. Compared to platform companies like Airbnb (where valuation focuses more on user growth), Cisco's valuation is more aligned with the hardware-driven AI training phase, but opportunities in enterprise AI cloud and network connectivity may be undervalued.

The 100% growth rate of AI orders is not reflected in the revenue guidance (6%). If the conversion rate improves, it will drive a valuation recovery.

Potential turning point for security business (new product orders up 20%, traditional products accounting for only one-third of total sales).

Overestimating risk: Corporate AI spending falls short of expectations (current revenue share <5%).

Strategic Judgment Platformization and Horizontal Expansion

Management's strategic focus on AI innovation and Splunk integration warrants further attention, such as HyperShield's addition of 750 new customers and its collaboration with NVIDIA on low-latency connectivity, signaling a shift toward platformization (expanding from hardware to AI-native software). However, a potential pitfall lies in passively responding to tariffs (assuming exemptions for semiconductors), and it is recommended to strengthen supply chain diversification. Horizontal expansion opportunities lie in sovereign AI and new cloud providers, analogous to the successful transition from routers to the security sector in the past. If the company increases investments in AI agents and threat landscape solutions, it may enter a new growth cycle.

Focus Areas 1. AI Full-Stack Integration: Silicon One chip + network OS + security HyperShield, integrated with NVIDIA/AMD ecosystems; 2. Sovereign Cloud Blue Ocean: Middle East/Europe collaboration projects (e.g., G42) to contribute revenue by 2026.

key variables

Positive catalyst:

AI order conversion rate (if H1 reaches 40%, revenue will be revised upward);

HyperShield penetration rate (new switch binding, currently 750 customers);

Increased share of sovereign cloud in RPO (currently undisclosed).

Early warning signal:

Enterprise routing/switching order growth rate (if <5%, it indicates AI delay);

Tariff exemption expires (impacting gross margin by 1-2 percentage points).

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Venus Reade·2025-08-14got in only a couple of years back around $50 due to Divy so far so good, for a long term investment. Will keep holding!!!1Report

- Merle Ted·2025-08-14I think we'll be up. Last quarter, I sold when it spiked at the opening. Perhaps some upgrades will help.1Report

- windy00·2025-08-14Incredible insights on Cisco's future! [Wow]1Report