Airbnb Soars Then Crashes: The $6 Billion Buyback Mystery

$Airbnb, Inc.(ABNB)$ The company reported strong earnings this quarter, with revenue exceeding expectations and net income falling significantly short of forecasts. It also announced a surprising $6 billion stock buyback program. However, the company's guidance for future growth was somewhat cautious, suggesting that the coming quarters may be challenging. The stock fell more than 7% in after-hours trading.

Looking specifically at the core information in the financial report

Revenue and profit

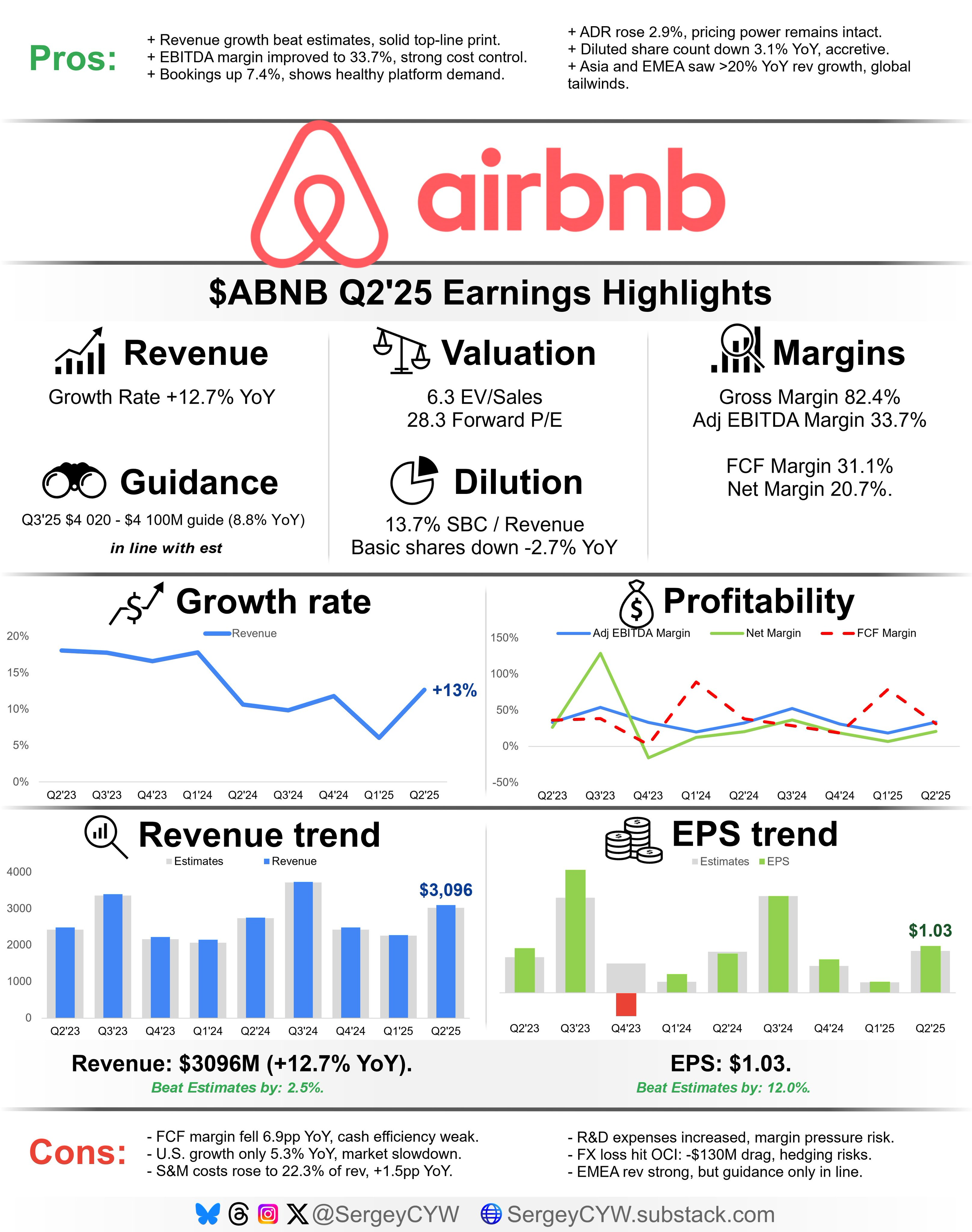

Q2 GAAP revenue: $3.1 billion, up 13% year-over-year, slightly exceeding market expectations (approximately $303 million).

Earnings per share: $1.03, a significant increase from $0.86 in the same period last year.

Operational efficiency and cash flow

Adjusted EBITDA reached $1 billion, maintaining a profit margin of approximately 34%. Free cash flow was also $1 billion, with a cumulative total of approximately $4.3 billion over the past 12 months.

The company has cash and cash equivalents of up to $11.4 billion, demonstrating its strong financial strength.

User and booking trends

The number of nights booked (Nights & Seats Booked) increased by 7% year-over-year; Gross Booking Value increased by 11% to $23.5 billion.

ADR (average daily rate) in North America rose by approximately 3%, while global ADR excluding foreign exchange rose by approximately 1%Reuters+1.

Product Expansion and Technology Application

The newly launched Services and updated Experiences have been well received, with AI chatbots reducing the need for human customer service by approximately 15%.

The CEO emphasized that Airbnb is transitioning toward an "AI-first" application approach, with the goal of becoming the "Amazon of the travel industry."

capital return strategy

Repurchased shares worth $1 billion; currently, there is still $1.5 billion of authorized repurchase authority unused, and an additional $6 billion repurchase plan has been approved.

About Future Guidance

The company's revenue guidance for Q3 is $40.2–41 billion, slightly above the average analyst estimate (approximately $40.5 billion), indicating that summer demand remains strong.

However, management warned that growth in subsequent quarters would slow due to comparisons with high base figures and macroeconomic uncertainties (such as US tariffs and new investment spending).

Key Investment Points

Airbnb is undergoing a transition from platform to brand.

From the current growth structure, Airbnb is evolving from an early "supply and demand matching platform" to a deeply branded "end-to-end travel experience brand." New products such as Services and the new version of Experiences signify its attempt to control more of the chain, thereby increasing average customer spending and customer loyalty. This is a major upgrade to its profit model and valuation system.

Investors should closely monitor whether these "non-property listing businesses" will bring about structural improvements in GMV in the future, rather than merely serving as traffic appendages.

AI strategy is an opportunity window, but it could also be a false proposition.

Management emphasized that Airbnb will transition into an "AI-first application" and launch an AI Agent with features such as automatic itinerary generation and intelligent customer service. This statement has undoubtedly attracted valuation premiums. A constructive view is that if AI can significantly improve customer service efficiency and customized service experiences, it could become a lever for improving retention rates. A cautious assessment is that current AI applications remain at a superficial support level, and achieving true product capability upgrades will require overcoming user habits, trust barriers, and data depth bottlenecks.

Stock buybacks send a signal, but do not necessarily indicate confidence in growth.

The $6 billion buyback program sends a strong signal that the company believes its stock price is undervalued, but it also exposes another reality: there are no higher-return capital allocation options available in the short term. For a tech company still in its expansion phase, this is a signal worth scrutinizing.

If growth momentum is insufficient and buybacks are merely a capital structure game, then long-term valuation digestion pressure will remain.

Valuations are at the "frontier of optimistic expectations," with the risk lying in the pace of realization.

Airbnb's current valuation (based on an expected EPS of approximately $5 for the full year 2025 and a P/E ratio of over 30 times) already reflects the pricing of "high-quality growth + platform expansion." The question is not whether this story is worthwhile, but whether the pace of realization matches expectations—if AI and new product penetration is slow, the risk of valuation correction will increase.

Investors need to watch two key variables

Variable 1: Has the GMV growth structure improved, particularly whether Experiences and the service layer contribute to total revenue?

Variable 2: Will long-term stays become a moat? If Airbnb can truly extend the user cycle, it will pose a differentiated threat to OTAs such as $Booking Holdings(BKNG)$ and $Expedia(EXPE)$ .

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Venus Reade·2025-08-08New price targets between $104-150. Averages out around $125. Premarket.. $122. Boom there it is.LikeReport

- SiliconTracker·2025-08-08Buyback looks big but stock still tanking lah, maybe market sees deeper issues?LikeReport

- Valerie Archibald·2025-08-08AirBnb is a great company, but it is a terrible stock to own.LikeReport

- UrsulaFowler·2025-08-07Interesting journeyLikeReport