$2.3B Buyback: Is Uber Saving Itself or Milking Investors?

$Uber(UBER)$ Q2 results exceeded expectations overall, but market expectations were also quite high, and the company's guidance for Q3 was relatively cautious (no big surprises), so there was no particularly strong performance after the market closed.

Two important trends in Q2:

Business structure optimization: Takeout becomes the main growth engine, offsetting the cyclical risks of transportation;

Strategic execution verification: Light-asset AV platform, membership economy, and global mergers and acquisitions form a synergistic closed loop.

In the short term, Uber needs to absorb the pressure on profit margins caused by technological investments, but the $23 billion buyback and free cash flow (more than 50% of which is used for shareholder returns) provide a safety cushion. In the long term, the valuation anchor will shift to the monopoly premium of the lifestyle services ecosystem and the profit-sharing potential of the AV platform, and the implied discount at the current price is expected to converge.

Key conclusion: Structural transformation is accelerating, and platform strategies are reshaping valuation logic, but pressure on profit margins is emerging.

Performance and market feedback

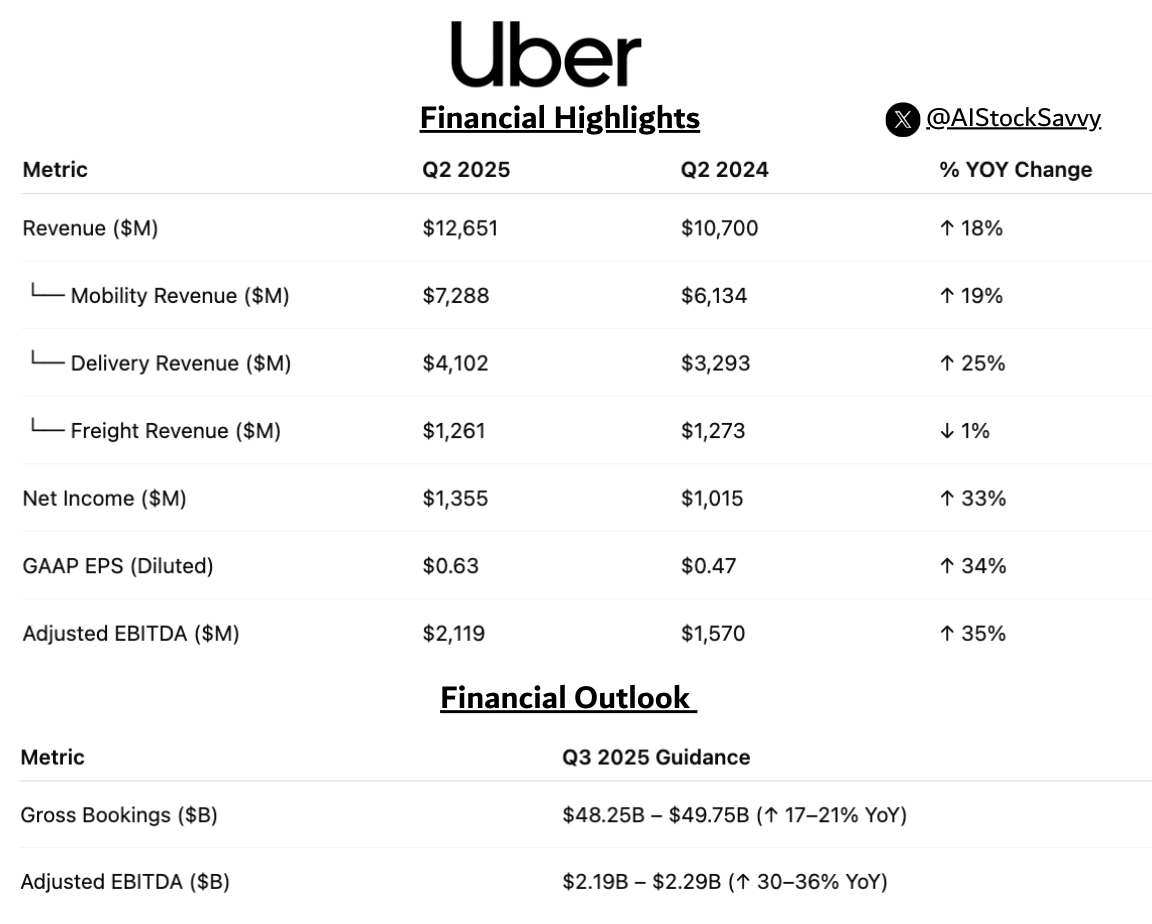

Key performance indicators

Stock price performance: Up 5% after hours (better-than-expected revenue + buyback catalyst), maintained +3% at the next day's opening.

Sentiment analysis: The market recognizes diversified growth and share buyback efforts, but there are differences of opinion regarding the slowdown in travel growth and the conservative EBITDA guidance.

Key Investment Points

Business structure transformation: food delivery overtakes transportation, membership economy becomes new engine

Delivery service:

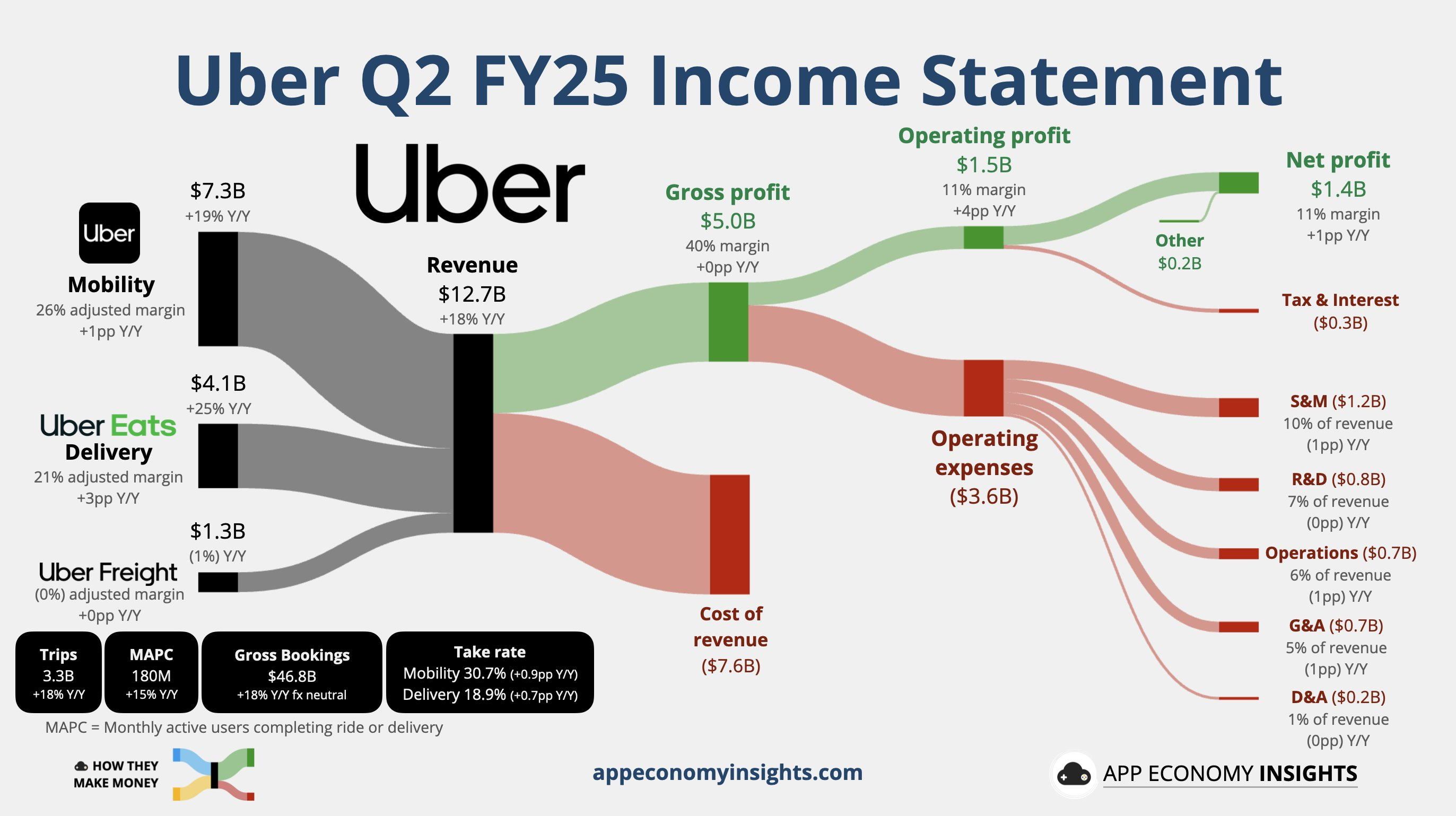

Order value: 21.73 billion (+2023.76 billion, +18% yoy), with the growth rate gap widening to 2 percentage points.

Driving force: Uber One membership reached 36 million (+60% yoy), contributing more than 40% of the platform's order value, with both renewal rates and ARPU on the rise.

Strategic significance: A highly sticky membership system reduces customer acquisition costs, supports long-term pricing power, and hedges against cyclical fluctuations in travel.

Concerns about a slowdown in the mobility business:

Order value growth slowed to +18% quarter-on-quarter from +20% in Q1, 0.6 percentage points below expectations, but trip volume increased by +19%, confirming the resilience of demand.

Countermeasures: Launch scenario-based features such as "women-only matching" and "senior mode" to increase penetration in niche markets.

Valuation Impact: The market pricing logic has shifted from "leading transportation company" to "super platform for lifestyle services," with the membership economy supporting PE premiums.

Autonomous driving: Light asset platform strategy opens up long-term ceiling

Model innovation: Abandoning heavy asset self-research and development, shifting to a third-party cooperation platform (Waymo/Baidu Apollo and 20 other partners). $Tesla Motors(TSLA)$

Verified results: In the Austin pilot program, Waymo vehicles received an average of more than 99% of human drivers per day.

Commercialization Path:

Merchant model (Uber bears the risk of monetizing traffic);

Agency model (revenue sharing);

Authorization model (investing $300 million in Lucid to develop hardware). ▶ Key expectations gap: The market underestimates the profitability of the platform revenue sharing model after AV scales up, which may contribute more than 20% of profits in the long term.

Financial Strategy: Aggressive Buybacks vs. Profit Margin Gamble

Share buyback scale exceeds expectations: An additional 20 billion in authorization, bringing the total buyback capacity to 23 billion (approximately 10% of market capitalization), signaling confidence in cash flow.

Profit margin pressure emerges:

Q2 adjusted EBITDA margin was 8.1%, but Q3 guidance implies a margin decline to 6.9% (mainly due to increased AI+ technology investments).

Wall Street interprets the divergence:

Bank of America Merrill Lynch: Conservative guidance, actual profits may be revised upward;

JPMorgan Chase: Necessary investment to maintain "scalability" assessment.

Valuation: Short-term profit pressure weighs on sentiment, but the $23 billion buyback plan forms a lower limit for share price support.

Competitive landscape: External threats are controllable, and ecological barriers are reinforced.

Tesla debunked: Management claims that the scale of its AV deployment is "extremely small" and has not affected market trends.

Moat in the food delivery sector:

Acquisition of Trendyol Go (Turkey) to strengthen regional coverage;

The Uber One membership system creates switching costs, suppressing the penetration of competitors such as DoorDash.

Expected revisions and valuation repricing triggers

Market Expectation Change Tracking

Key variables for revaluation

Positive Catalysis:

Uber One membership exceeds 50 million (currently 36 million), validating the scale effect of the subscription model.

The proportion of orders from AV cooperation platforms has increased to over 5%, confirming the feasibility of the revenue sharing model.

Downside risks:

Technological investments have resulted in EBITDA margins consistently below 8%.

Weak macroeconomic consumption has suppressed the growth rate of travel orders to below 15%. $Lyft, Inc.(LYFT)$

Institutional Viewpoints

$Bank of America(BAC)$ (Buy, TP $115): Significant valuation discount (2026E FCF 23x vs FANG 46x), membership + AV strategy not fully priced in.

$JPMorgan Chase(JPM)$ (Overweight): Improved credit safety margin and EBITDA scalability support the logic of rising stocks and bonds.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- EVBullMusketeer·2025-08-08Buyback cushion helps, but margins pinch near-term. Long-term ecosystem play still on trackLikeReport

- BelindaHaywood·2025-08-07Intriguing analysisLikeReport