August Ambush: When FOMO Dies, OMO Strikes

Combined with ETF flows, repurchase activity, institutional positions and sentiment indicators, the capital structure of the U.S. stock market in August is gradually entering a "wait-and-see + defense" phase from the previous state of full attack.Although it does not mean that the market will immediately turn short, but the marginal weakening of the driving force of capital, coupled with the seasonal pullback tendency, making the market more sensitive to risk. $S&P 500(.SPX)$ $SPDR S&P 500 ETF Trust(SPY)$ $NASDAQ(.IXIC)$ $Invesco QQQ(QQQ)$

Against the backdrop of a lack of sustained incremental buying, the market could adjust quickly in the event of a bearish catalyst, such as a rebound in economic data, a geo-event or a hawkish Fed statement.Therefore, it is recommended that investors pay close attention to the trend of capital flows and changes in the configuration structure, to grasp the rhythm to control positions.

Net capital inflow trend in August showed signs of slowing down

Since the beginning of the year, the U.S. stock market has attracted a large amount of capital inflows, especially concentrated in the technology giants as the representative of the "seven heavyweights", as well as AI, semiconductor-related thematic ETFs.However, in August, the pace of capital inflows cooled down significantly.According to ETF fund flow data, although the total amount is still positive, the frequency of daily net inflows has decreased, while there is a small increase in the number of net outflow days.This change may reflect the market's rising skepticism about the short-term upside of U.S. stocks, with investors choosing to partially cash in gains or engage in structural rotation at higher levels.

Core dynamic quantitative strategies (systematic and momentum trading) remain the mainstay of funds, but with a shift in demand structure.Systematic funds' global allocation to U.S. equities is expected to rise to the 65th percentile, triggering $48 billion in passive buying if markets are flat

Fund flows have shifted from a full spread to a "select track", showing tech stocks accounting for 72% of new allocations (up from 63% in June) (Microsoft/Apple or pushed up by algorithmic trading); at the same time, the energy sector has been sharply underweighted, and there has been a systematic sell-off in commodity-related cyclicals, exacerbating the sectoral divergence

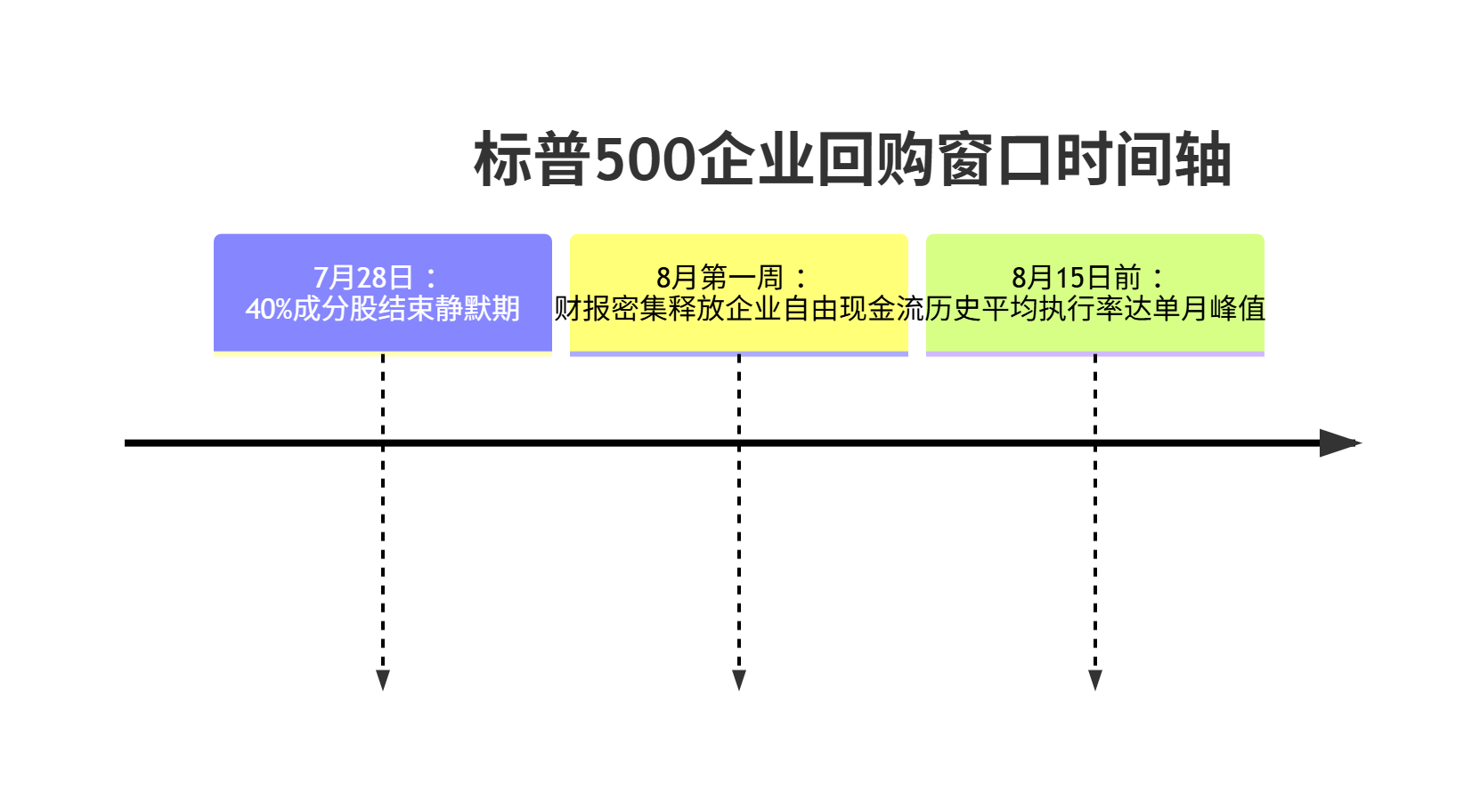

Corporate buybacks are key support at the end of the quiet period

Corporate buybacks are a non-negligible driving force in the flow of U.S. stock funds, especially in the S&P 500 constituent companies, accounting for a significant portion of total annual capital requirements.But with the end of the earnings season, buyback behavior by the SEC regulations will enter the "quiet period".This means that in August the market lost part of the "natural buying" support, net capital inflow pressure may intensify.Historical experience shows that stock market volatility tends to rise during the repurchase window closure, and the probability of a pullback increases.

According to the folding chart data, the size of corporate pending repurchase execution reached a daily average of $1.8 billion (+37% from July), of which the technology giants accounted for 51% ( $Apple(AAPL)$ $Alphabet(GOOG)$ after the earnings or accelerate the repurchase), the financial sector repurchase efforts increased abruptly (chart shows that the amount of repurchase authorization of bank stocks +22% year-on-year)

If the market pulls back 3%-5%, buyback behavior will form technical support, but need to be wary of the rising cost of corporate debt (interest rate sensitivity at a decade high) to weaken the long-term buyback capacity

Institutional allocation tends to be conservative, incremental capital wait-and-see sentiment rises

In terms of position allocation, a number of large funds and CTAs (Commodity Trading Advisors) had reached relatively high exposure levels by the end of July.In the absence of a clear favorable driving background, August is more of a "defensive rebalancing", such as health care, consumer necessities and other low-beta sector reallocation, as well as technology stocks, cyclical stocks, a moderate reduction in positions.Behind this "active cooling" operation is the concern about the uncertainty of economic data and the ambiguity of the policy path, leading to more cautious new funds.

Market sentiment is overheated, triggering the migration of capital risk aversion

Changes in capital flows in early August were highly correlated with changes in investor sentiment. the AAII survey showed a sharp rise in the proportion of retail investors who were bearish, while the VIX options market showed low hedging demand.Often when sentiment is extremely optimistic, funds are more likely to flow out of risky assets and into safer assets (such as bonds or money market funds).This type of short-term risk aversion is not a systematic withdrawal, but it is enough to create structural pressure on indices and amplify price volatility against a backdrop of low volume.

And derivatives darkened under the retail retreat.Top stock basket inflows declined for the third consecutive week, as seasonality (summer vacations) + valuation pressures caused retail investors to turn to money funds (yields broke 5%)

On the other hand, single-stock options trading volume surged, the implied volatility curve took on a "bimodal shape" - tech calls (betting on earnings) vs. index puts (hedging against systemic risk), with the put/call volume ratio rising to 0.89 (prior) and the put premium hitting a 6-month high of 0.82.0.82) and put premiums hit a 6-month high, revealing a surge in hedging demand

U.S. bond yield volatility creates disruption to equity fund flows

The recent rebound in U.S. bond yields, especially the 10-year Treasury yield which once approached 4.2%, has narrowed the risk premium between the equity and bond markets.For long-term funds (such as pension funds, insurance funds), when the risk-free rate of return is attractive enough, their willingness to allocate to equities will decline.This "asset reallocation" tendency was particularly evident in August, with some U.S. equity ETFs showing signs of capital outflows, especially in the interest rate-sensitive growth sector.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- zookie·2025-07-29Great insights! Love the analysis! [Wow]LikeReport

- snappix·2025-07-29Incredible insights! Thanks for sharing! [WOW]LikeReport