Gold is standing at a critical turning point after a 2.5-month deep pullback of up to 20% to 25%.

On June 15th, Barclays and Citigroup spoke out on the same day. The former clearly shouted that "it is time to increase gold exposure", while the latter raised the three-month gold price target price from $4,000/oz to $4,500/oz. Common judgment of the two institutions:This correction is more like a price reset than the end of a bull market.

The core catalyst for this round of optimism is the announcement that the United States and Iran will formally sign a memorandum of understanding (MoU) on Friday. According to Citi Research, this event is expected to push the Strait of Hormuz trade flow to basically return to normal in mid-to-late July, and the oil market will refocus on weak supply and demand fundamentals-Citi lowered its Brent crude oil forecast from the third quarter of 2026 to 2027 to $75, $70 and $65/barrel respectively (previous forecasts were $110, $90 and $80/barrel).

Citi believes that after geopolitical tensions ease, inflationary pressures will tend to ease, and the key macro headwinds that previously dragged down gold prices may gradually fade. At the same time, Citi maintained its bullish forecast of $5,000/oz for 6 to 12 months, but it indicated that the gold price still faced the risk of large volatility.

Barclays' comprehensive review of this round of decline from three dimensions: exchange rate, stock strategy and derivatives. The bank believes that the double suppression of the US dollar strengthening by about 2.5% and the S&P 500 index rising by more than 10%, combined with the centralized clearance of crowded long positions, jointly led to this rapid adjustment.However, the medium-term support is intact: high inflation, persistent policy uncertainty and the strategic need for diversified reserves of central banks will re-dominate the trend of gold prices once geopolitical pressures stabilize. According to Barclays' estimate, for every 1 percentage point increase in US CPI, the price of gold will rise by about 5%. This inflation transmission mechanism will constitute the core driving force of this round of rebound.

US-Iran Memorandum of Understanding: Key Catalysts Enter, Oil Price Expectations Are Comprehensively Reversed

The breakthrough in U.S. -Iran talks is seen as one of the most important commodity market events of the year, according to Citi Research. Citi pointed out that the market has now digested the news of the signing itself, but has not yet fully priced the scenario of sustained flow recovery in the Strait of Hormuz in the medium term-Otherwise, the current crude oil price should be about $10 to $15/barrel lower than the current level, which means that there is still room for further downside in oil prices.

Citi's benchmark scenario (probability 60%) is: after the MoU is formally signed, the negotiations will continue to advance, and the oil market will have a paper supply surplus of about 4 million barrels/day by 2027, and the crude oil price will probably fall below 70 USD/barrel by then. At the same time, Citi has set two tail scenarios: a bull market scenario (with a probability of 20%), where the situation briefly eases and then conflict breaks out again; The bear market scenario (probability 20%) is the rapid increase of production capacity in the UAE, Saudi Arabia and Iran and the implementation of the Russia-Ukraine ceasefire agreement.

The spillover effect of falling oil prices directly benefits precious metals.Citi believes,The energy inflation shock brought by the conflict in the Middle East is one of the important root causes of the previous pressure on gold prices-high oil prices push up inflation expectations, thus forcing the central bank to maintain a hawkish stance and suppress the downside of real interest rates. As the pressure on oil prices eases, this transmission chain is expected to gradually reverse, opening an upward channel for gold prices.

Barclays: This round of adjustment is a "reset", not an end

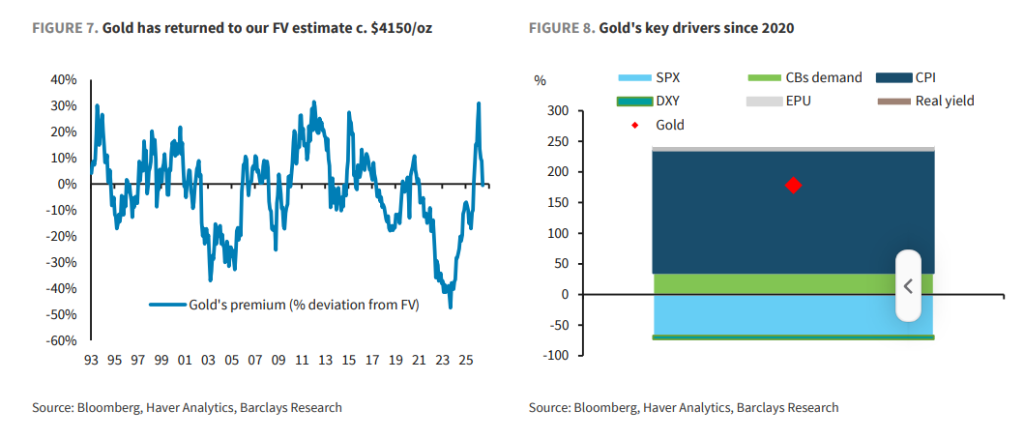

According to Barclays Research, gold has increased by more than 100% cumulatively since January 2024. After surging to about $5,500/oz in January this year, it immediately experienced a pullback of about 25%, pulling the price back to November 2025 levels. Barclays pointed out that this round of adjustment is not surprising considering the previous high technical extension and the obvious overrise of relative macro factors (especially real interest rates).

From a valuation perspective, the Barclays team said,Gold prices have returned to the range estimated by the bank's fair value model of about $4,150/oz. The model lists U.S. CPI, S&P 500, the US Dollar Index and central bank gold purchase demand as the four core drivers of gold prices. Since the beginning of this year, the US dollar and the stock market have strengthened together, which has negatively suppressed gold; At the same time, some emerging market central banks sold gold reserves during the Middle East conflict to stabilize their currencies, bringing additional selling pressure, further depressing the price of gold.

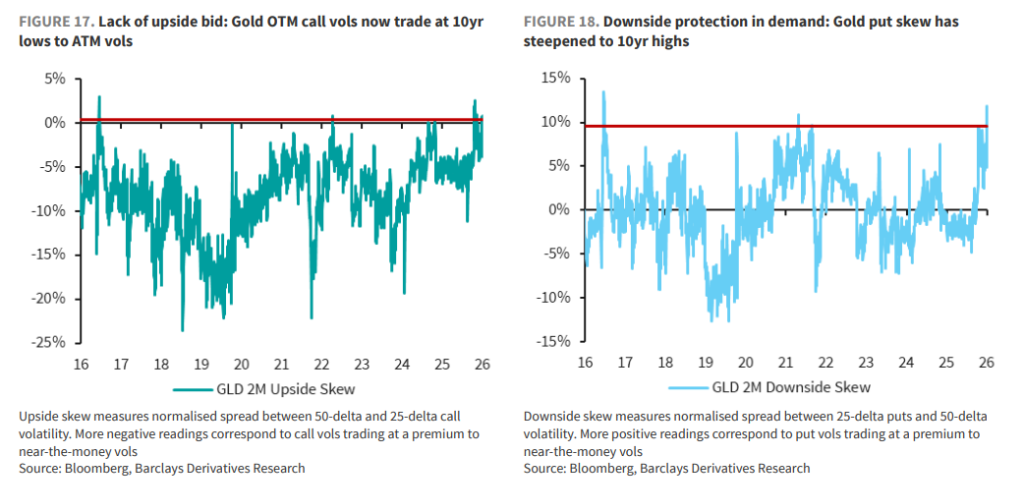

At the option market level, according to the Barclays Derivatives Strategy team, market positions and options pricing indicators have significantly normalized from extreme levels at the beginning of the year.

Most noteworthy: Call implied volatility has reversed from a deep premium at the beginning of the year to its lowest level in nearly a decade, while put skewness has risen to a near-decade high due to a pick-up in hedging demand. This structural shift means that,The cost performance of capturing asymmetric returns through options has been greatly improved, and the overall clearance of market sentiment has also laid a healthier technical foundation for the new round of upward movement.

Long Tail Effect of Inflation: The Strongest Structural Support of Gold Price

Barclays sees U.S. inflation as the dominant variable in gold's medium-and long-term movement.

Its model estimates,For every 1 percentage point increase in CPI in the United States, the price of gold will rise by about 5%, which means that the cumulative push-up effect of energy shock in the Middle East on CPI will be embedded in the upward logic of gold price for a long time in the form of persistent inflation even after the oil price finally falls.

In a more macroscopic structural perspective, Barclays believes that multiple long-term benefits remain intact.

First, the trend of de-dollarization continues to evolve, gradually eroding the demand for US dollar reserves.

Second, the long-term tendency of central banks in developed markets to tolerate inflation levels slightly above the target will continue to erode the purchasing power of fiat currency.

Third, the expectation of currency depreciation brought by fiscal deficit expansion and tariff policy gives gold additional premium support beyond historical correlation.

The central bank's gold purchase data also shows that structural demand remains stable.

According to the latest data of the World Gold Council (WGC), in the first quarter of 2026, the central bank's gold purchases (in ounces) increased by 17% quarter-on-quarter, and in US dollars, they increased by 38% quarter-on-quarter due to high gold prices. In the first quarter, the main buyers were the central banks of Poland and Uzbekistan, and Tether, the world's largest stablecoin issuer, also continued to increase its positions. In the first quarter, it purchased 12.6 tons, and the total reserve rose to 154 tons, ranking fourth in the world, surpassing most major central banks. Turkey and Russia saw massive net sales due to the demand to stabilize their local currencies. Barclays believes that as geopolitical tensions stabilize, emerging market central banks that previously sold gold reserves are expected to restart their overweight.

Comments