The global memory chip industry is undergoing a historic paradigm shift: it is transforming from a traditional "skyrocketing" cyclical commodity to a highly deterministic strategic resource for AI infrastructure. The core impact lies in the complete subversion of the valuation framework-Leapfrog from traditional price-to-book ratio (P/B) to P/E (P/E).

On June 1st, according to the news of Chasing Wind Trading Station,Goldman SachsIn the latest in-depth research report of the global semiconductor storage industry,The current upstream cycle of memory chips is different from the past. AI-driven demand persistence, constrained supply growth and structural changes in long-term supply agreements (LTAs) are driving the storage industry from a high-cyclical commodity track to an AI infrastructure track with predictable profits.

The report pointed out that four disruptive changes are undergoing in the fundamentals and valuation logic of the industry:

First, the gap between supply and demand was revised upward across the boardIn 2027, the supply tightness of the three major markets of DRAM, NAND and HBM will exceed that of 2026, and the shortage will continue into 2028;

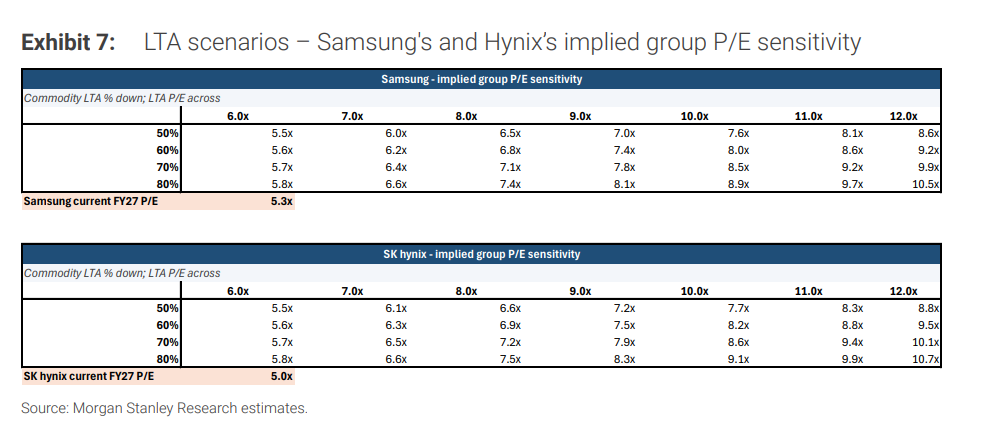

Secondly, the valuation framework has undergone a historic switchThe industry benchmark officially shifted from price-to-book ratio (P/B) to P/E (P/E), driving the target price of the "Big Three" to increase sharply across the board (Hynix implies about 53% upside,Samsungimplied about 60%);

Third, HBM's pricing logic revaluationIn 2027, the average price of HBM will achieve a "catch-up compensatory increase" of up to 44% to ordinary DRAM, and its global market size (TAM) will be revised up by 54% to US$116 billion in 2027;

Finally, the medium and long-term operating profit forecasts of the Big Three have been revised up across the board, high profit margins will be throughout the forecast period.

Coincidentally, before Goldman Sachs, the big Wall Street investment banksMorgan StanleyAndJPMorgan ChasePointing to the same judgment in the latest research report:Storage giants represented by Samsung and SK Hynix are standing at the historical node of valuation paradigm switching.

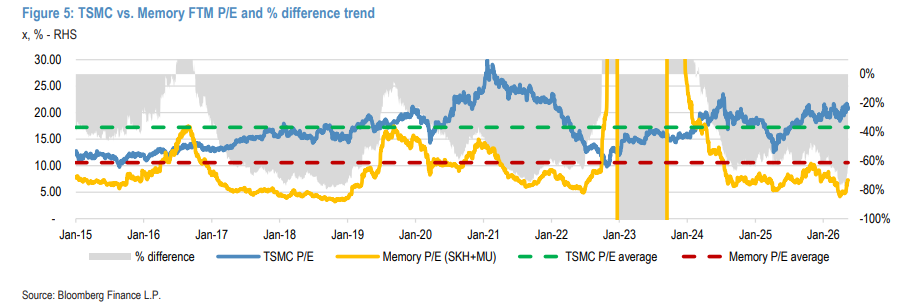

Morgan Stanley and Xiaomo believe that the large-scale landing of long-term supply agreements (LTAs) is expected to push the market to reprice these companies from "strong cyclical products" to "technological infrastructure with stable cash flow attributes". At present, the storage giant's forward P/E is only about 7.3 times, which is the same asTSMCThere is a 50% – 80% valuation discount between.

Three structural anomalies: Why will this cycle run at a high level for a long time?

The current cycle has completely deviated from the historical trajectory of 2017-2018 driven by the single point of cloud data center. Goldman believes that the underlying logic of fundamentals is being reshaped by three structural forces:

Demand side: AI server takes over absolute dominance

The cyclical drag of consumer electronics has been thoroughly marginalized. Data shows that servers will account for about 50% of DRAM and 40% of NAND demand in the whole industry in 2025; It will climb further to 61% and 43% by 2028. The global server memory market size in 2025 (approximately $449 billion) is already 7.4 times that of 2017.

With the evolution of large language models (LLMs) to enterprise AI agents (Agentic AI), Token consumption is expected to reach more than 24 times of the current processing capacity by 2030, and memory bandwidth and capacity have become the core bottlenecks constraining the development of AI.

Supply side: HBM capacity "devouring" effect intensifies

Traditional storage expansion is being rigidly constrained by physical conditions. The wafer capacity required for HBM production is 3-4 times that of ordinary DRAM. As HBM iterates to HBM4 and HBM4E, the ratio of wafers consumed per unit product continues to climb.

Between 2026 and 2030, approximately 30% of the available cleanroom capacity of the three major original plants totaling approximately 1.39-1.54 million tablets per month will be forcibly locked in for HBM production. This will cause the supply of traditional DRAM to shrink significantly to 15% CAGR from 19% in 2017-2018.

Business Model: Long-Term Supply Agreements (LTAs) Reshape Earnings Certainty

Storage factories and hyperscale cloud vendors are systematically suppressing cyclical fluctuations through LTA. At present, there is clear financial evidence in the industry:SanDiskThe 3Q26 financial report disclosed that its new business model agreement has included US$42 billion in deferred revenue obligations (RPO) and US$400 million in advance payments, with penalties for default.

The history of the silicon wafer industry shows that the widespread popularity of LTA can give the oligopolistic industry extremely high profit stability, which has also become the core cornerstone supporting the storage sector to enjoy a higher valuation multiple.

Supply and Demand Gap Data Penetration: Facing More Severe Shortages in 2027

The data shows that the supply and demand gap of the three major categories in 2027 has not only not been bridged, but has further deteriorated compared with 2026:

DRAM:The supply-demand gap in 2026/2027/2028 fell deep to-5.0%, -5.9% and-3.9%, respectively. Driven by the strong demand for server DRAM, the year-on-year growth rate of the average price of traditional DRAM in 2026 is expected to be as high as 326%, and the operating profit margin will reach the historical extreme value of about 80%.

NAND:The gap between supply and demand was-4.4%, -4.6%, and-3.0%, respectively. The demand for enterprise-grade SSD (eSSD) will surge by 66% and 31% in 2026 and 2027, respectively, driving NAND operating margin to maintain a high range of 60%.

HBM:Shortages were the most deadly, with gaps of-5.4%, -6.0% and-4.3%, respectively. Goldman Sachs predicts that the HBM market size will reach US$56 billion, US$116 billion and US$168 billion in 2026, 2027 and 2028, respectively, due to the sudden rise in demand on the ASIC side (with a growth rate of 172% in 2026).

Abandoning PB and Embracing PE: A Leapfrog Upward Revision of the Target Price of the "Big Three"

Based on the qualitative change in earnings visibility, Goldman's pricing of storage stocks has officially anchored a P/E multiple (based on 9x):

SK Hynix (Buy):The price target jumped to a range of 3.3 million to 3.5 million won. The stress test shows that even in the face of the extremely negative situation of price drop of 30% for two consecutive years, its profit margin can still be maintained at a healthy level of 40%, thoroughly falsifying the old logic of "the peak of the cycle means loss".

Samsung Electronics(Buy):The price target was raised to 480,000 won. Operating profit in 2026 is expected to grow more than 8x year-over-year, with ROE hitting an all-time high of 52%. Its HBM revenue will soar to about $44 billion in 2027.

But it's worth noting that storage price hikes are backing down the stream, with operating margins in Samsung's smartphone division expected to collapse from 11% to an all-time low of 2%.

Kioxia (Upgraded to Buy):The 12-month price target was set at JPY 93,000 based on FY3/28E earnings of 7.8x P/E under NAND expectations of "longer highs".

Wall Street Consensus Assembly: How Morgan Stanley and Morgan Stanley Think of Valuation Framework Switching

This valuation paradigm shift from P/B to P/E is not an isolated judgment of a single institution. The latest judgment of Morgan Stanley and JPMorgan Chase has also formed a strong resonance.

According to a previous article on Wall Street, Morgan Stanley clearly pointed out that memory has become the absolute bottleneck of AI infrastructure. Long-term supply agreements (LTAs) are turning traditional strong-cycle businesses into long-arm cash flows with rigid guarantees and high margins.

If the market continues to price ordinary cyclical products in the same way it treats them, there will be a serious valuation misalignment. Quantitative calculation shows that in the neutral case (100% coverage of LTA by HBM, 70% coverage of ordinary memory and 10 times P/E), the implied overall P/E of Samsung and Hynix should reach 8.5-8.6 times; If the LTA coverage is increased to 80%, the implied P/E will exceed 10.5 times.

JPMorgan Chase's logic directly hits the essence of the business game: The buyer's fear of cutting off supply and the seller's fear of demand default together contribute to the legally binding long-term agreement.

The agency also offered a radical bullish command:Samsung's target price was raised to 480,000 won (corresponding to 8 times P/E), SK Hynix was raised to 3 million won, and Kioxia's target price was directly doubled to 80,000 yen.

It is worth noting that the three top institutions on Wall Street have unanimously pointed the frame of reference to TSMC: 2014 bindingAppleAfter the long-term agreement, TSMC successfully switched the valuation framework to P/E, and maintained it in the range of 10-30 times for a long time.

At present, the storage giants, whose forward P/E is only about 7.3 times, are facing a historic narrowing opportunity with a valuation discount of up to 50%-80% with TSMC.

At the same time, however, Wall Street retained its last cold bottom line:The contract is not literal enough to fully immunize the cycle.At the end of the 2017 cycle, forward agreements were reduced to waste paper in just a few months after demand collapsed.

This time, the only ironclad evidence that can really support the new valuation framework is that real money advances and legally locked deferred income obligations must appear on the balance sheet. Without real cash inflow escort, everything about the grand narrative of crossing cycles, will be just a mirage.

Comments