PPL Corp (NYSE:PPL) on Friday reported better-than-expected earnings for the first quarter.

The company posted quarterly earnings of 63 cents per share which beat the analyst consensus estimate of 62 cents per share. The company reported quarterly sales of $2.774 billion which beat the analyst consensus estimate of $2.668 billion.

PPL affirmed FY2026 adjusted EPS guidance of $1.90-$1.98.

“Our first-quarter results reflect strong financial and operational results and keep us on track to achieve our 2026 earnings guidance range,” said Vincent Sorgi, PPL president and chief executive officer. “We’re on pace to complete $5.1 billion in 2026 infrastructure investments to strengthen and modernize our electric and gas networks, build new generation resources in Kentucky and improve customer service while maintaining affordability for our customers.”

PPL shares rose 0.6% to trade at $36.12 on Monday.

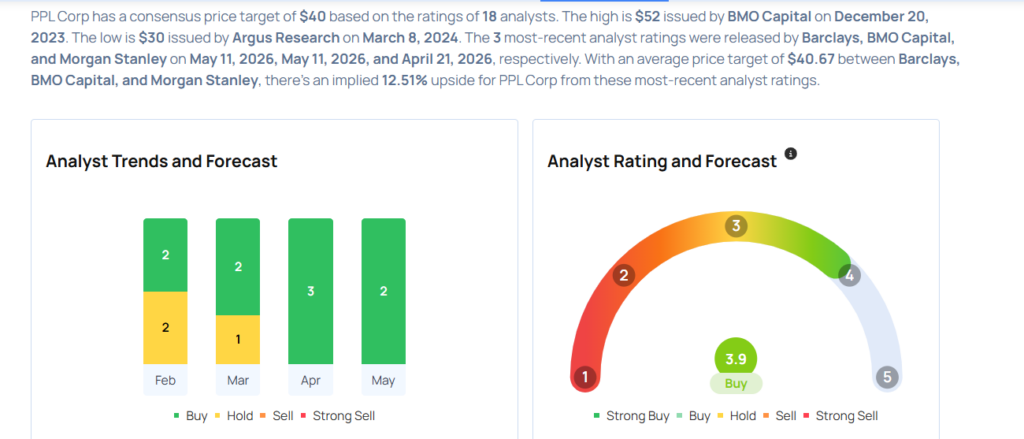

These analysts made changes to their price targets on PPL following earnings announcement.

- BMO Capital analyst James Thalacker maintained PPL with an Outperform rating and lowered the price target from $42 to $40.

- Barclays analyst Theresa Chen maintained the stock with an Overweight rating and cut the price target from $41 to $39.

Considering buying PPL stock? Here’s what analysts think:

Photo via Shutterstock

Comments